The War is Over… April Fool

Momentum is a high volatility strategy. The Iran war has proved it.

No Assets Spared

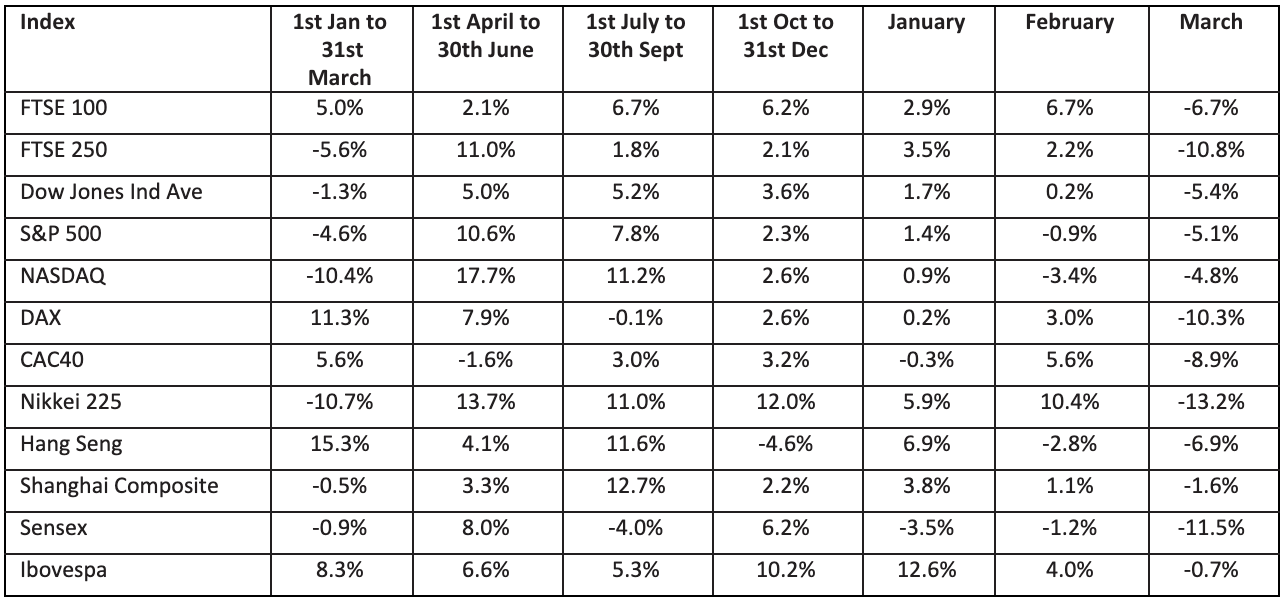

With the exception of oil and gas stocks, no sector has been spared. Bearish sentiment about the impact of the oil shock has been exacerbated by leveraged trading. As investors have unwound positions, selling of liquid asset – bonds, gold has been substantial. It is interesting to see how the impact of the war closely mirrors previous conflicts.

Unfortunately, this doesn’t give us much of an indicator of what will happen next. The two extremes of the scenarios are:

- Peace breaks out with a resumption of traffic through the Straits of Hormuz, everything slowly goes “back to normal,” but with inflation higher for a period as oil production normalises. This favourable outcome may take a long time to come about as so much capacity has been damaged in Russia and in the UAE

- War continues leading to more damage to infrastructure and leads to a long-term disruption of traffic in the Gulf of Hormuz. A global recession follows as oil prices spike and shortages occur globally. Europe will soon start running low on jet fuel. Asian countries are already rationing

There are of course many other possibilities between these two extremes.

The market’s response on the 31st to hopes of a deal has been dramatic with a strong bounce in lots of markets:

Some of those very badly hit – gold, for example has bounced.

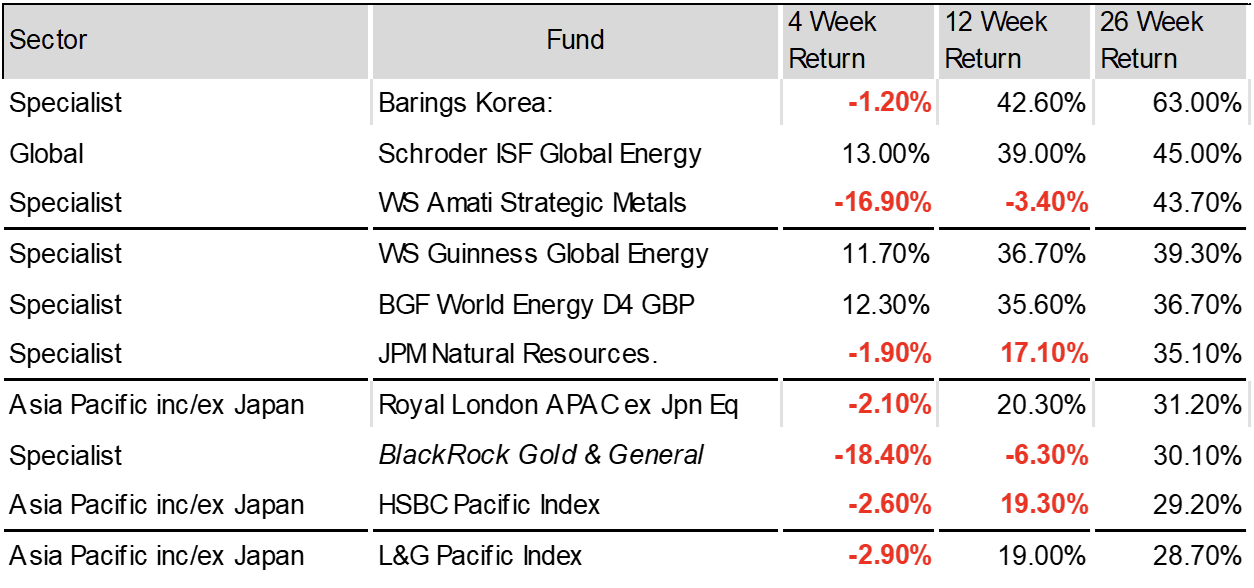

The best performers over the last 26 weeks

Source: Morningstar

We can see the strength of the bounce in those funds which went into the war with the strongest momentum:

A week ago, Barings Korea was down 11.5% since our last blog. Today, a week later, as you will see above, it is only down 1.2%. Royal London APAC ex Japan is a similar story. Gold which was slowing down has not recovered so well.

Oil and gas?

The only winner of the month is, of course, oil.

The performance of last month’s portfolio is a salutary lesson in the problem of human interference in what is essentially an algorithmic process: I undertook, when we began 20 months ago, to pick four funds all with strong momentum but aiming to diversify. Unconsciously discounting the possibility of an actual war when I selected, I missed out a February momentum winner – oil and gas, which then went on to be the best performer in March. I did so on the basis that Oil up would not be a sustained trend. Oh dear. Fire that fund manager!

The Great Rotation is Still Alive

The implications of all this is that if war stops, then the momentum we were following will reassert itself.

If the war stops.

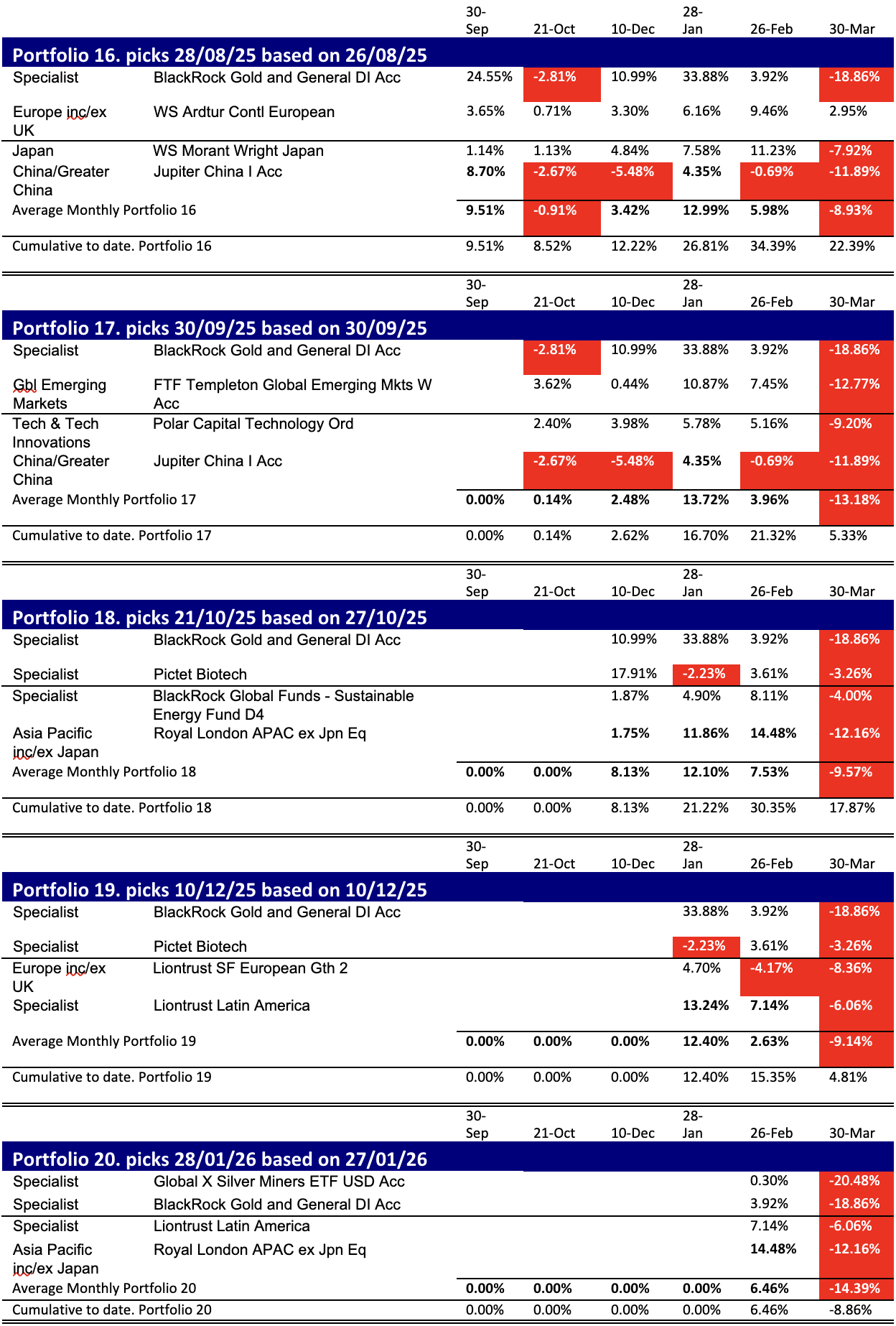

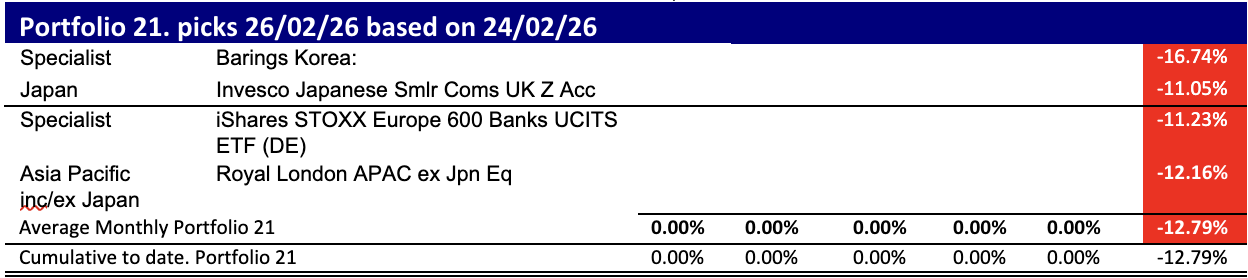

Our Portfolios

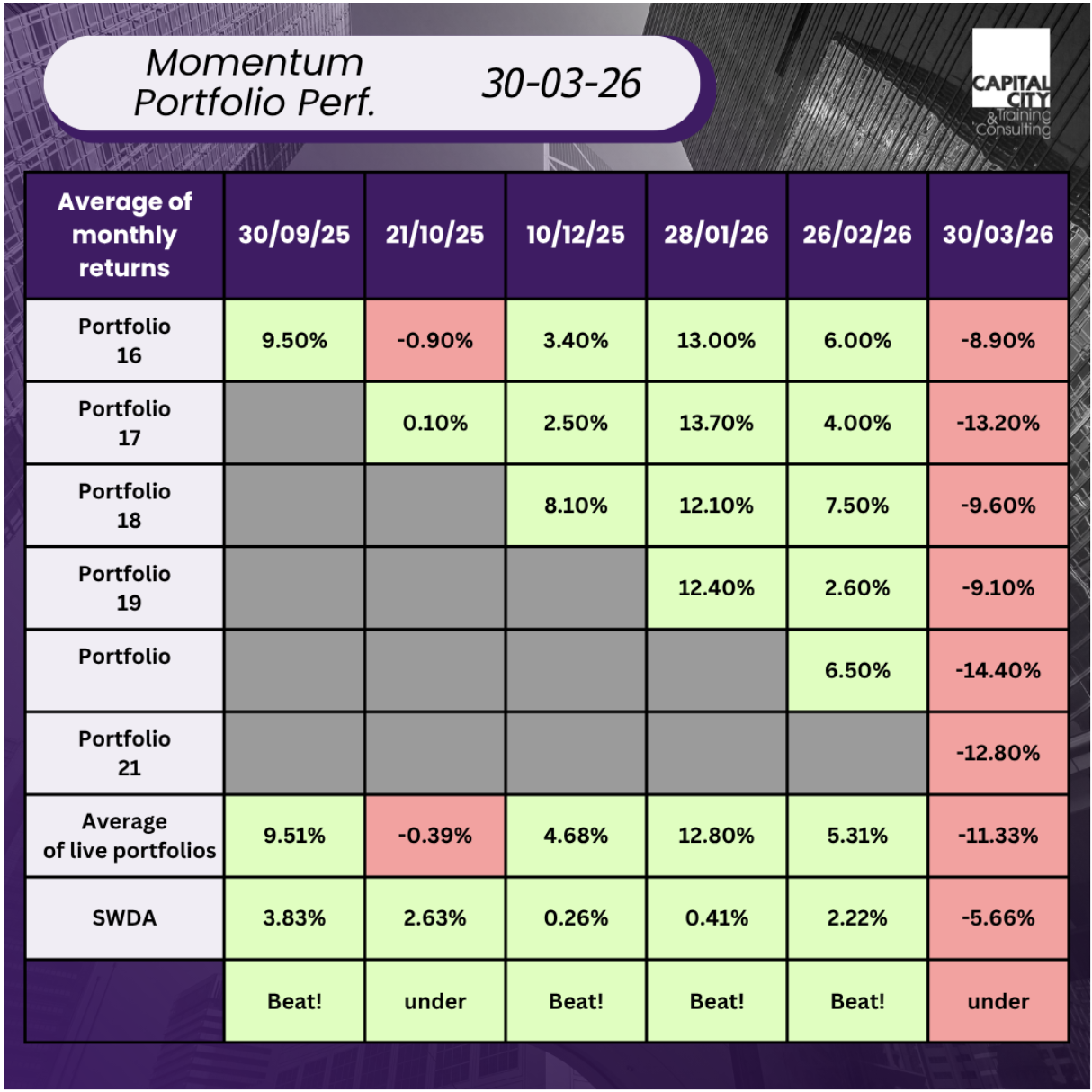

So how have the portfolios performed?

The great relative performance has stopped. We’ve beaten SWDA in four out of the last six months!

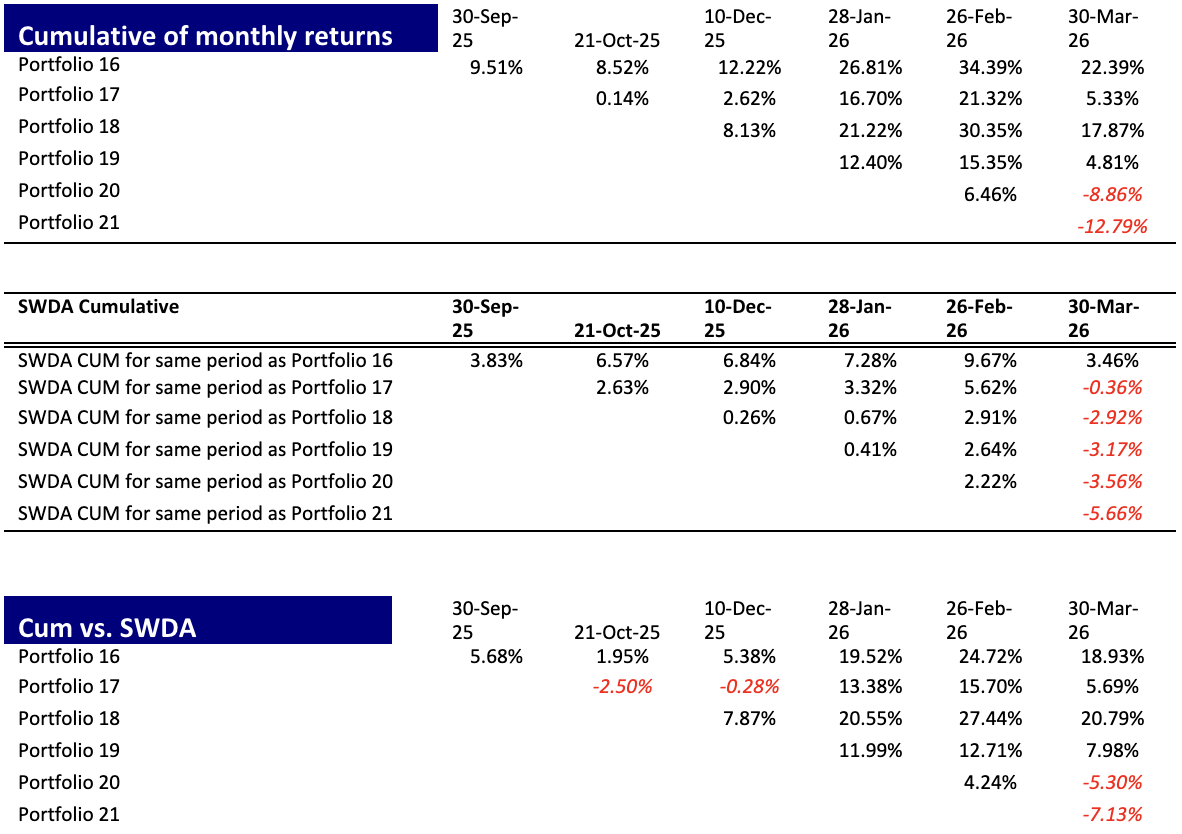

Is there value in the strategy? The following tables shows 1) cumulative returns of the SWDA Index and 2) the relative cumulative performance of each fund over the same horizon in each case. As you can see five out of 6 portfolios have outperformed on a cumulative basis.

How have the individual portfolios performed?

Is now the time to be starting a momentum portfolio?

Given market momentum over the last month, perhaps the appropriate portfolio is a short portfolio? It is an idea worth considering and we should think about the two extreme scenarios, one will let February’s momentum reassert itself, the other will lead to a potential bear market.

The question is “Does it make sense to take the risk of taking on an equity position today, when we can earn 4% plus in Government bonds or higher if we take risk on in areas like floating rate mortgage-backed securities?”

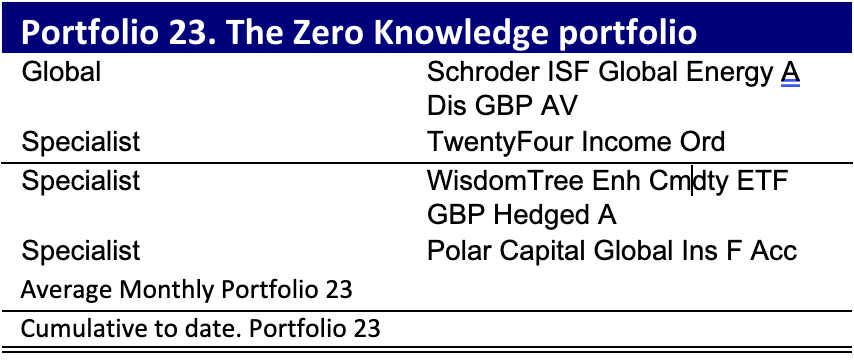

Another way to ask this question is “If we are completely ignorant about the outcome of the war, what mix of assets will do us the least harm? What zero knowledge portfolio makes sense?”

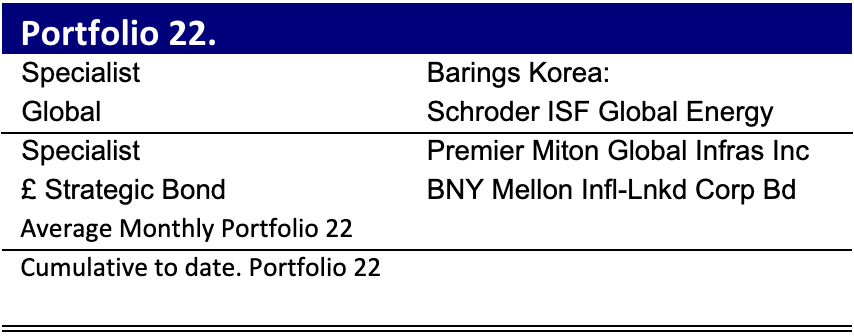

Momentum in March and a new portfolio Twenty one

With the zero-knowledge portfolio in mind, there are some obvious asset classes to choose:

- Oil and Gas

- Inflation – i.e. broad commodities, one thing we do know is inflation will be higher.

- Mortgage-backed securities (subordinated) high return and although we may see poor price performance short run, we can earn high yields (c. 10% dividend yields)

- Insurance – returns are not correlated with the broader market or cyclical (in the classical sense)

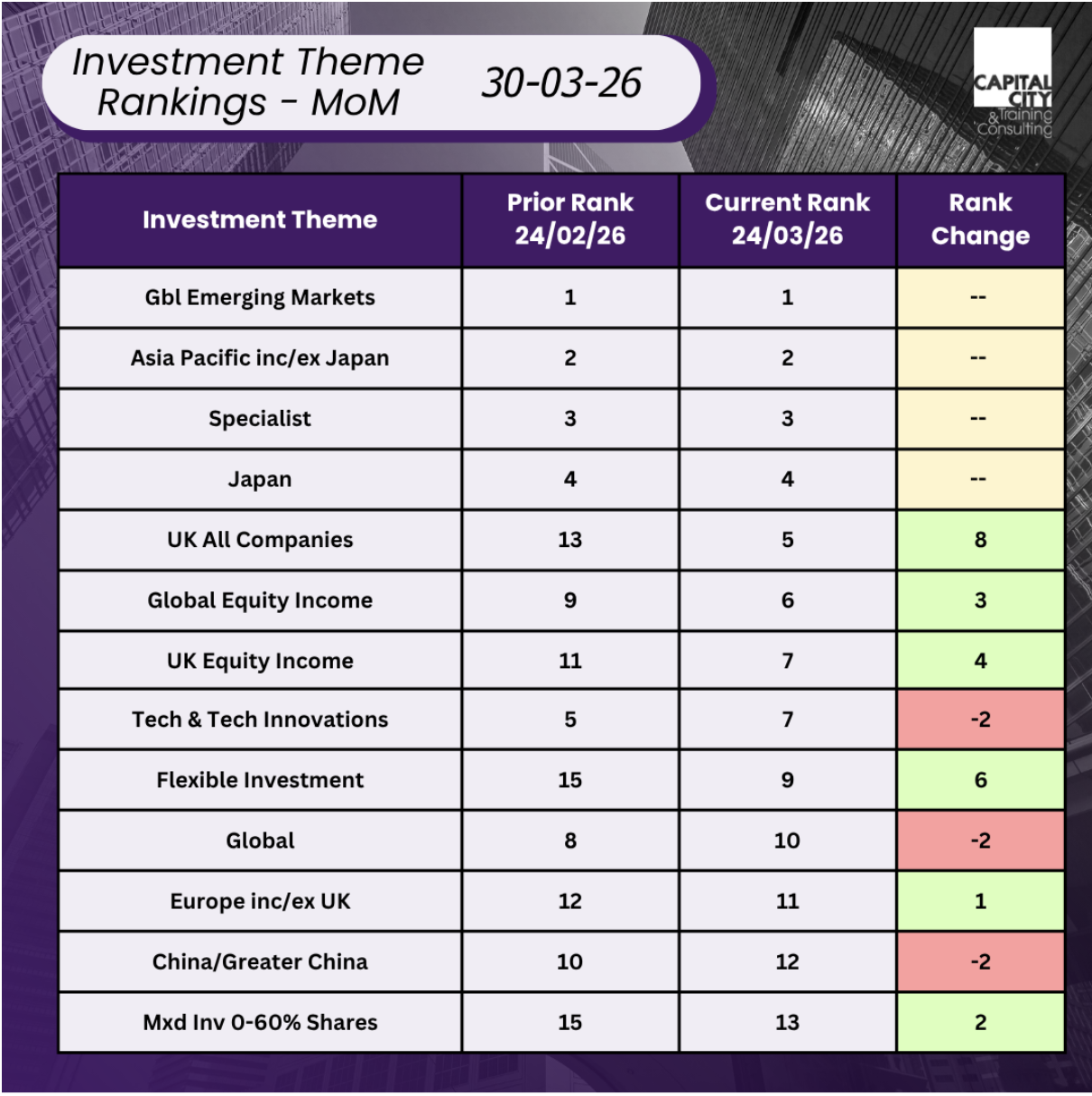

If we look at the momentum summary below, the picture is a little distorted – the Specialist energy funds are the top performers, so on a weighted basis – this “specialist” category would be number one. Specialist includes a lot of poor performers this month – gold and metals in particular. Global emerging markets have not “performed” in the classical sense; they have merely fallen less than their peers.

This month I will suggest two strategies – one will be my “No knowledge portfolio,” the other will be a conventional one following our usual strategy, i.e. assuming that war resolves and pre-war momentum reasserts itself.

This month’s portfolios

find us on substack & Youtube

access the data for yourself

Former banker turned entrepreneur. I successfully restructured, purchased, managed and sold a private engineering group, Steel Line Ltd, through an LBO and was also an equity partner in Corporate Training Group which my partners and I successfully sold to the AIM listed ILX group in 2006. I established Capital City Training Limited in early 2010 with my business partner Greg. We acquired MS Consultants a few years ago (so I’m still doing a bit of M&A). I have had non-exec roles for a small and growing VA/recruitment business and a fast-growing beverage logistics company. I am also an active investor.

Capital City Training is a full service technical and management development training company focused on the banking, wealth management and broader financial services and accounting industries. Having said all that, in the last couple of years we’ve been branching out into training for non-financial companies – manufacturing, retail, tech, defense.. so old and new economy. We also provide consultancy around modelling and are currently working for a leading PPP/PFI advisory firm. We have delivered training in every continent of the world in 2024… except Antarctica. Perhaps in 2025?! Watch this space.

Capital’s dedicated faculty combine extensive line experience as corporate financiers, bankers, traders, portfolio managers and equity analysts together with over 60 years of experience in learning and development as both procurers and providers of tailored in-house training, eLearning and blended learning. Our faculty also includes experienced Management development training specialists allowing us to provide HR consultancy services, management development training and also innovative integrated management development & technical training events. Capital City’s faculty embody over 100 years of line experience across the fields of accounting, corporate finance, derivatives, credit, lending, investment, equity research transaction banking and origination.