The war is not over… but the markets act like it is

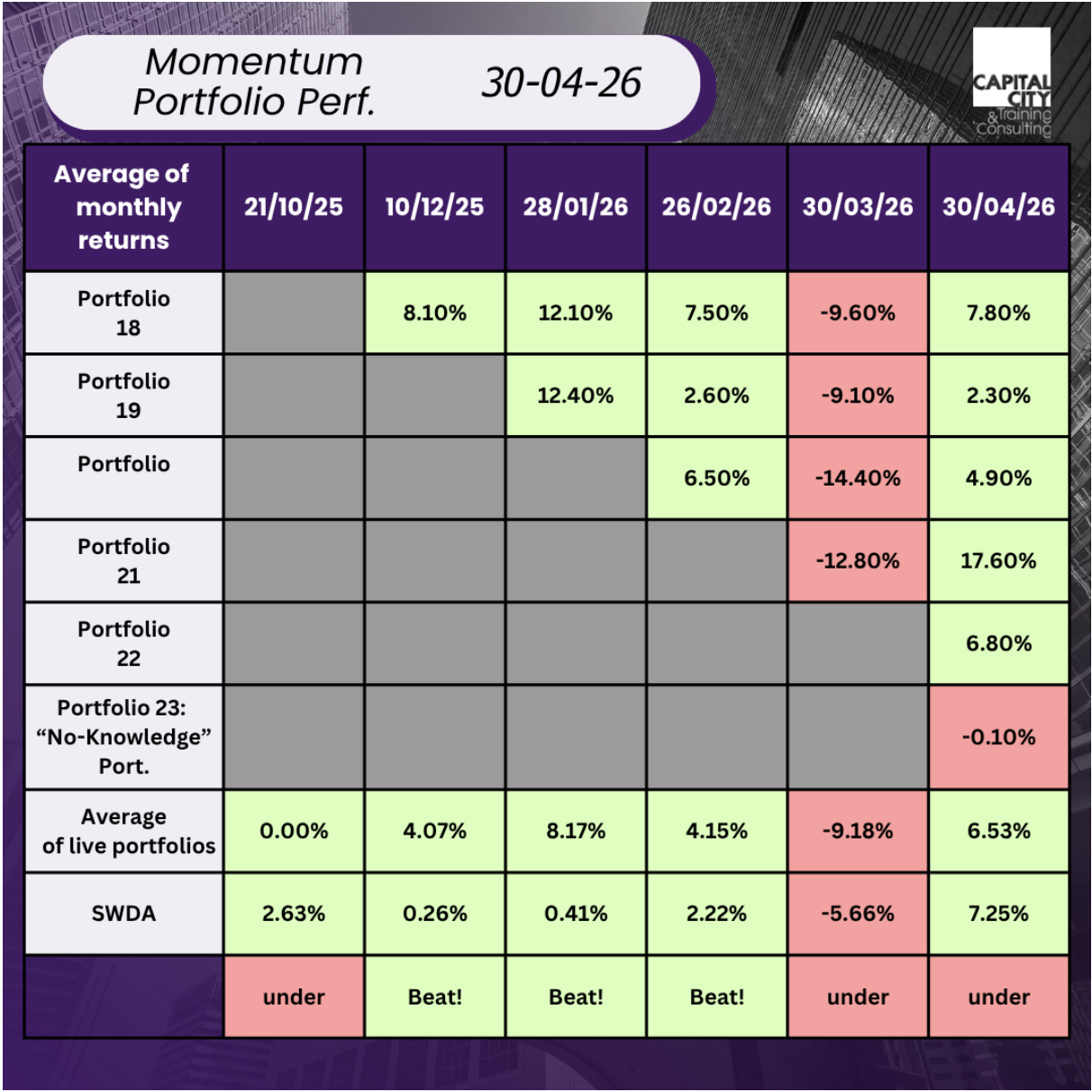

Momentum Reasserts Itself…

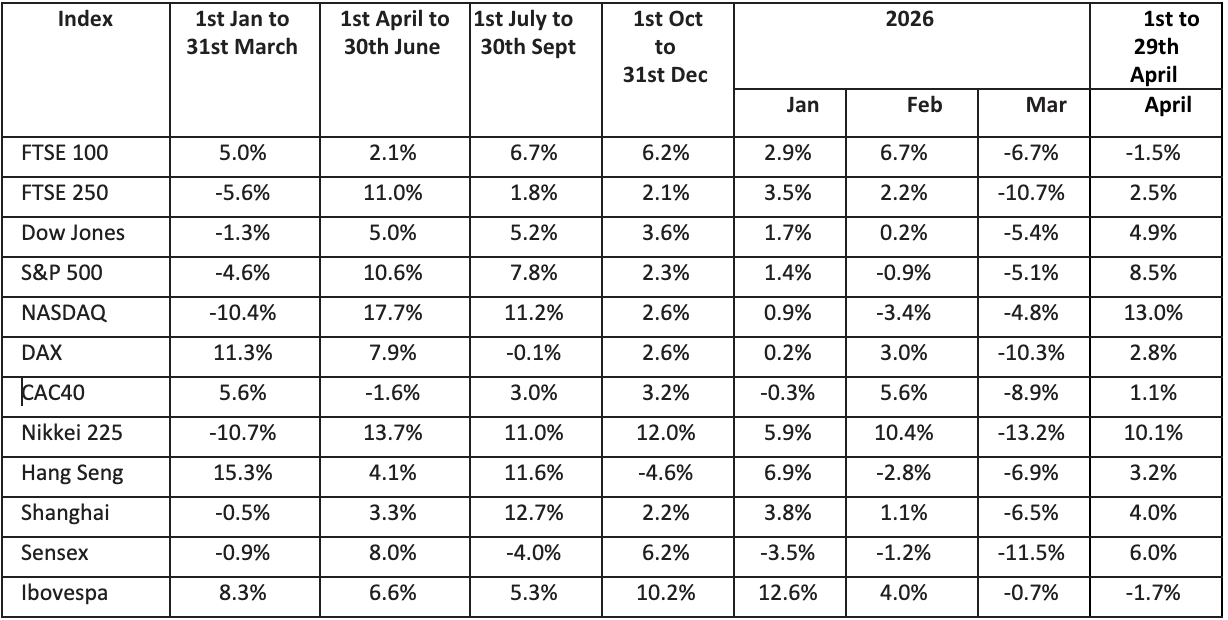

The month of April has seen a big reversal and recovery – albeit not uniform: technology, the US market and Asia have all recovered strongly. The EU and UK not so much. Precious metals have also been lacklustre (no pun intended).

Wow

The story I have heard from traders is that two forces collided this month: short positions taken up by hedge funds met liquidity coming into the market. Fund managers deploying this caused a lot of short covering and a consequential big bounce. The WSJ also had an interesting article suggesting that markets are behaving differently, driven in large part by a new generation of day traders who fledged during lockdown.

Their “Buy the dip don’t sell the rip” approach and the way multi-strategy hedge funds are organised appears to have changed how corrections play out.

The press has also gone from being dominated by the war pre-ceasefire, to instead return to the focus on tech and AI. Markets were talked down around Spotify, up over Nvidia, then down over OpenAI, then up over positive results from Alphabet. As we discussed in previous months, the performance of the Mag7 is diverging. IS OpenAI looking like a loser in the AI race?

The net positive form these big tech plays have helped propel the S&P500 to a new record at month end.

Who would have thought?

The story appears to follow the momentum! If we look further afield, linked to the technology issue is Korea with our pick from last month returning 28.5% having fallen 16.74% the previous month. Remember “Buy the dip don’t sell the rip.”

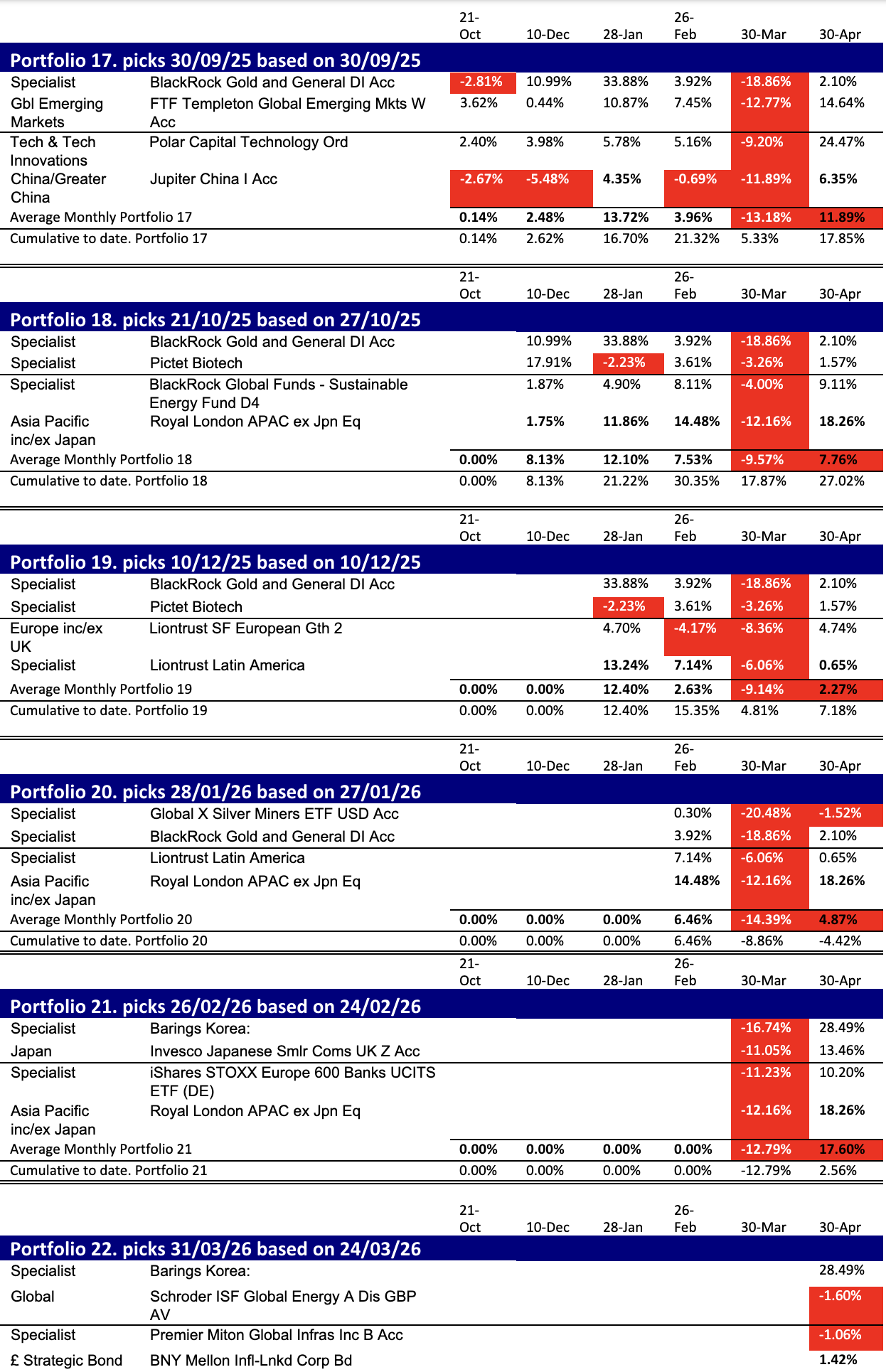

Source: Morningstar

We can see the strength of the bounce in those funds which went into the war with the strongest momentum:

A week ago, Barings Korea was down 11.5% since our last blog. Today, a week later, as you will see above, it is only down 1.2%. Royal London APAC ex Japan is a similar story. Gold which was slowing down has not recovered so well.

Oil and gas?

The momentum has gone from oil for the time being, with late April’s peak having been lost and then largely reclaimed as negotiations in the Gulf have stalled.

The great rotation is splitting

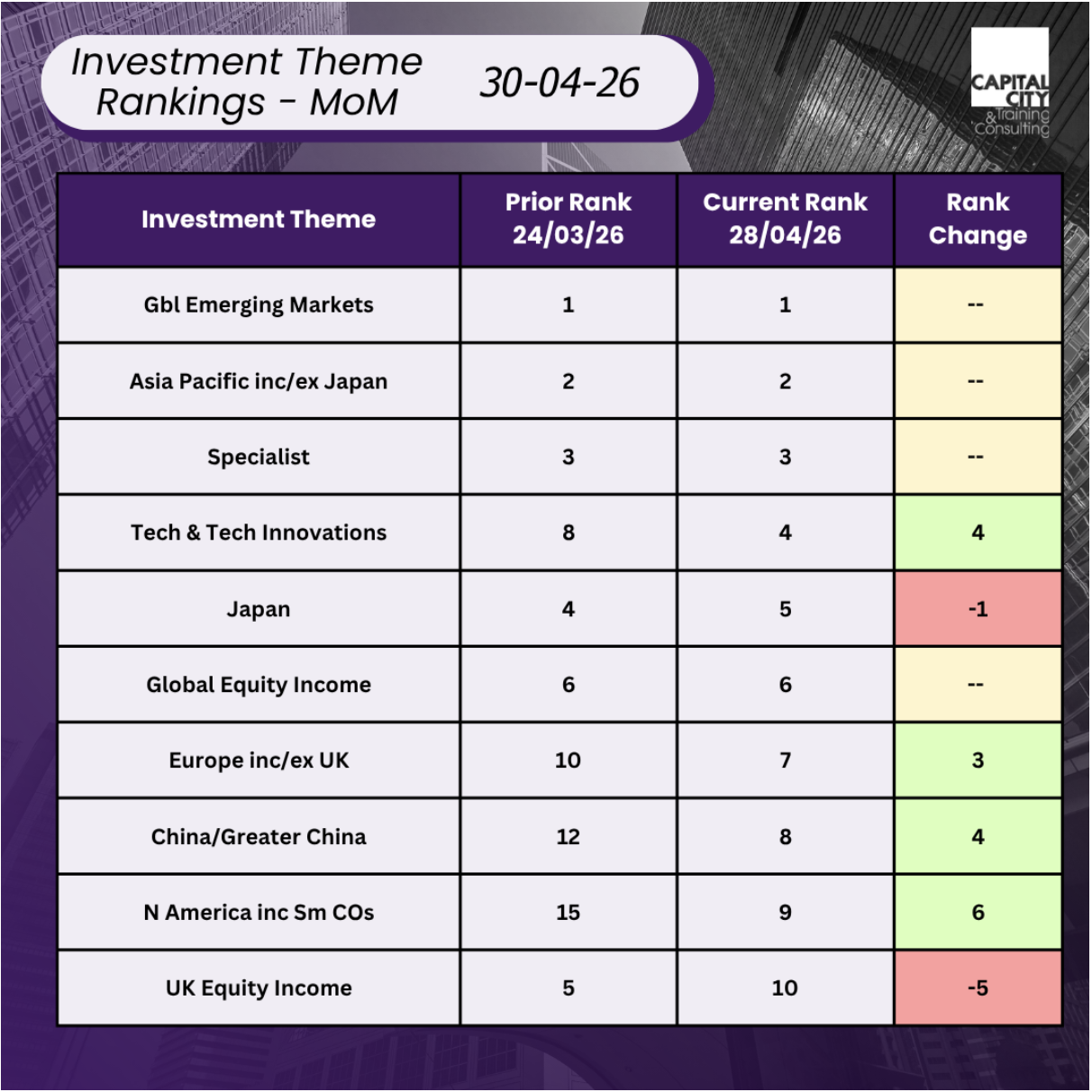

We said last month that it seemed likely that the longer-term momentum would reassert itself after the war. The bounce has borne this out in part, but Asian stocks have outperformed Latin America. We must remember though that a big part of the Asia story and large cap story is tech; this is very definitely the case in Korea. If we look at our top 10 funds for the month, we are focused in tech and Asia growth.

Broader metal – Not precious metals

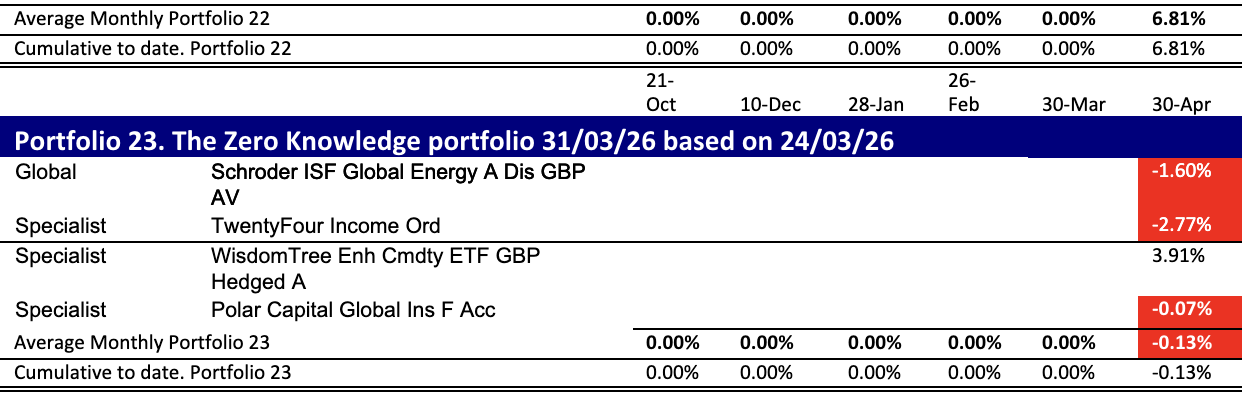

An interesting story in the top 10 is Amati Strategic Metals. Whereas gold, silver and related miners have gone flat or suffered (the miners!) in the last month, Amati has not. This reflects the fact that whilst 60% of its portfolio is in gold and silver miners it has significant exposure to a broader group, including copper, lithium, nickel, manganese, platinum group, and rare earth metals.

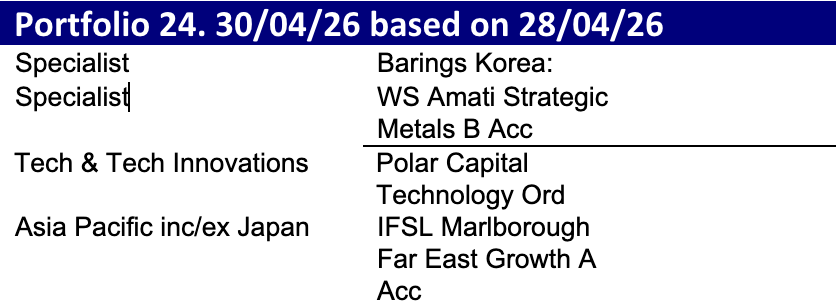

Our Portfolios

So how have the portfolios performed?

How have the individual portfolios performed?

Momentum in April and a New Portfolio Twenty-One

If we look at the momentum over the last four weeks, then the ranking would be:

- Tech

- Korea (sort of tech)

- European opportunities

- Global emerging markets

If we take the pure momentum approach, allocating as per the 4-week momentum picture is not inconsistent with the 6-month momentum picture. The 6-month picture would have given us:

- Korea

- Strategic metals

- Technology

- Asia Growth

Given the lack of broader momentum in Europe, I think it is fair to treat the European opportunities fund as a red herring.

This month’s portfolios

find us on substack & Youtube

access the data for yourself

Former banker turned entrepreneur. I successfully restructured, purchased, managed and sold a private engineering group, Steel Line Ltd, through an LBO and was also an equity partner in Corporate Training Group which my partners and I successfully sold to the AIM listed ILX group in 2006. I established Capital City Training Limited in early 2010 with my business partner Greg. We acquired MS Consultants a few years ago (so I’m still doing a bit of M&A). I have had non-exec roles for a small and growing VA/recruitment business and a fast-growing beverage logistics company. I am also an active investor.

Capital City Training is a full service technical and management development training company focused on the banking, wealth management and broader financial services and accounting industries. Having said all that, in the last couple of years we’ve been branching out into training for non-financial companies – manufacturing, retail, tech, defense.. so old and new economy. We also provide consultancy around modelling and are currently working for a leading PPP/PFI advisory firm. We have delivered training in every continent of the world in 2024… except Antarctica. Perhaps in 2025?! Watch this space.

Capital’s dedicated faculty combine extensive line experience as corporate financiers, bankers, traders, portfolio managers and equity analysts together with over 60 years of experience in learning and development as both procurers and providers of tailored in-house training, eLearning and blended learning. Our faculty also includes experienced Management development training specialists allowing us to provide HR consultancy services, management development training and also innovative integrated management development & technical training events. Capital City’s faculty embody over 100 years of line experience across the fields of accounting, corporate finance, derivatives, credit, lending, investment, equity research transaction banking and origination.