The world waits for a peace deal… tech stocks? They just don’t care

Did the war with Iran really happen?

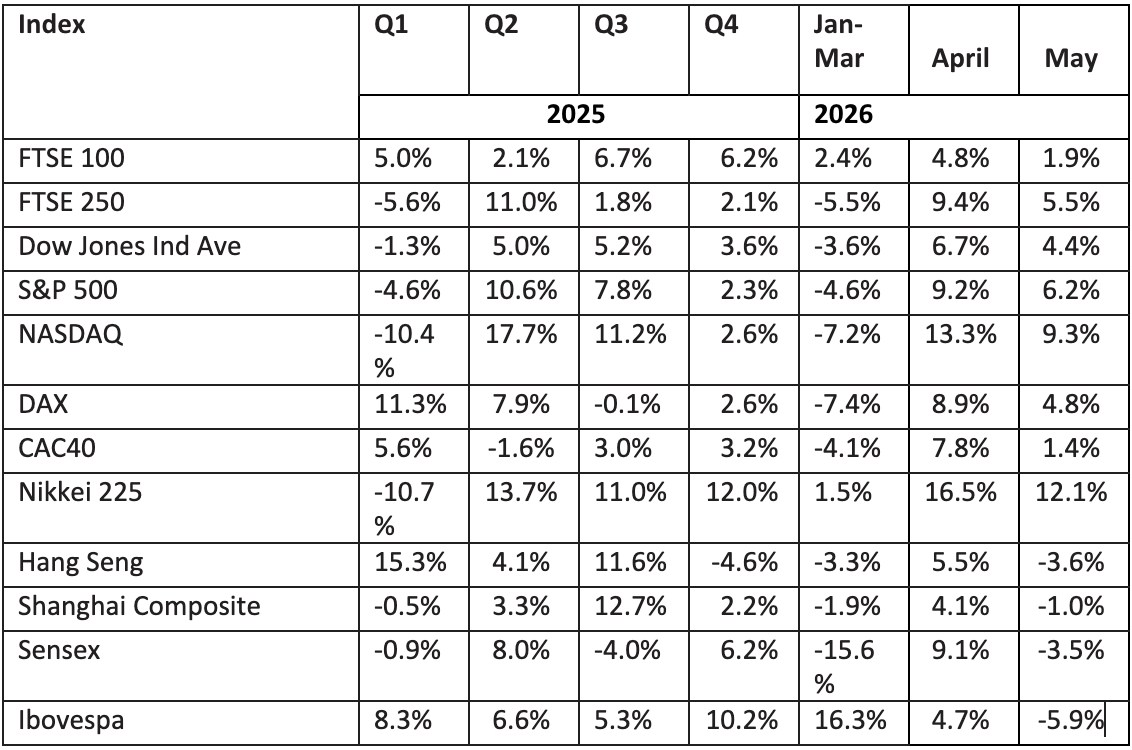

Markets have recovered from the impact of the Gulf war and then some. With the exception of Brazil and India (a heavy importer of oil from the gulf), markets have had another very strong month. Higher oil prices and their potential longer-term impact are being ignored, for now.

Tech is the “hidden” driver across EM

Last month we talked about short covering and new money coming into the market and how the market stepped up and down with each news release from the Tech majors. In May there was no “bad news” in Tech, everything just pushed prices higher: Alphabet’s mega raise was met with equanimity. The price target for SpaceX’s IPO went even higher.

Nvidia went into the PC market, Anthropic made preliminary filings for its trillion-dollar IPO and Micron Technology doubled in value to over $1 trillion in only 48 days!

If the tone sounds breathless, that is how the market is feeling!

All momentum is concentrated in Tech at the moment, specifically AI stocks and their supply chains.

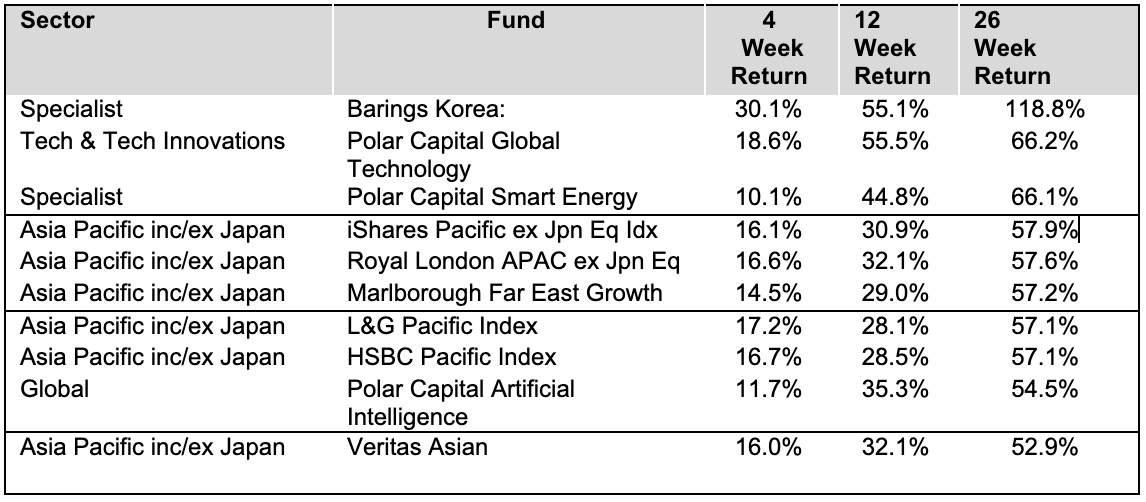

The best performers over the last 26 weeks

Source: Morningstar

We can see this in the top 10: Korea – Barings Korea has over 1/3 of its fund in AI supply chain technology stocks. Similarly, the iShares Pacific ex Japan is nearly 20% invested in Taiwan Semiconductor (TSC). 14% is in Korea’s Samsung Electronics and SK Hynix.

Oil and gas?

The momentum has gone from oil for the time being, with late April’s peak having been lost and then largely reclaimed as negotiations in the Gulf have stalled.

The great rotation was splitting

Has the longer-term momentum started to reassert itself? No. instead we have technology driven Asian markets performing spectacularly. Korea, Taiwan, Japan but less so Hong Kong. Latin America – has no tech (except for NuBank (Nu Holdings) and Meli – neither are AI. January’s pick, Liontrust Latin America, has gone backwards in May (2.56%). No AI.

Commodities and metals

Whilst precious metals have been subdued over the month, Copper is up over 10% and this has given the mining sector a good month. Again, we see technology supply chain at work. In the same way that the USD/JPY is down significantly over the year to date – from 142-160, precious metals fell and then have been flat as money has flowed back to USD. Precious metals and their miners have no (or maybe negative) momentum for now.

Pan African Resources is an interesting example: it raised gold production 40% in the year (albeit at the bottom of the range of expectation), hit production cost targets and has expanded reserves through its low-cost merger of its exploration JV partner Emerson. The shares trade on a forecast P/E of 6.3x and a PEG of 0.1X. On the day of the announcement the share fell from 139p to 115p. They now stand at 110p. Resolution of the war will probably be needed to change this momentum.

Oil and broad commodities are slightly down – WCOB, part of our zero-knowledge portfolio is down 1.26% over the month. An interesting question now is what will be the longer-term impact of oil prices as the world struggles to normalise post a reopening of Hormuz?

The head of Exxon believes $150 per barrel oil prices are coming and will stay for a significant period as reduced supply due to damaged infrastructure and inventory rebuilding push up prices.

Warnings signs that the market is ignoring

It is very easy to argue that markets are in a state of euphoria over tech: compute will become commoditised just as fibre optic capacity did.

However, there are many indicators also flashing red: Consumer confidence is at very low levels in the US.

Inflation is very real, and credit card delinquency is high. Valuations are just not sustainable:

It is questionable as to what levers the US Government can use to combat recession and high inflation – stagflation – in the US if current consumer trends continue. Perhaps money printing, cutting short term rates, issuing gold-backed treasury bonds, and debasing the US dollar will be the only, if unpalatable options open.

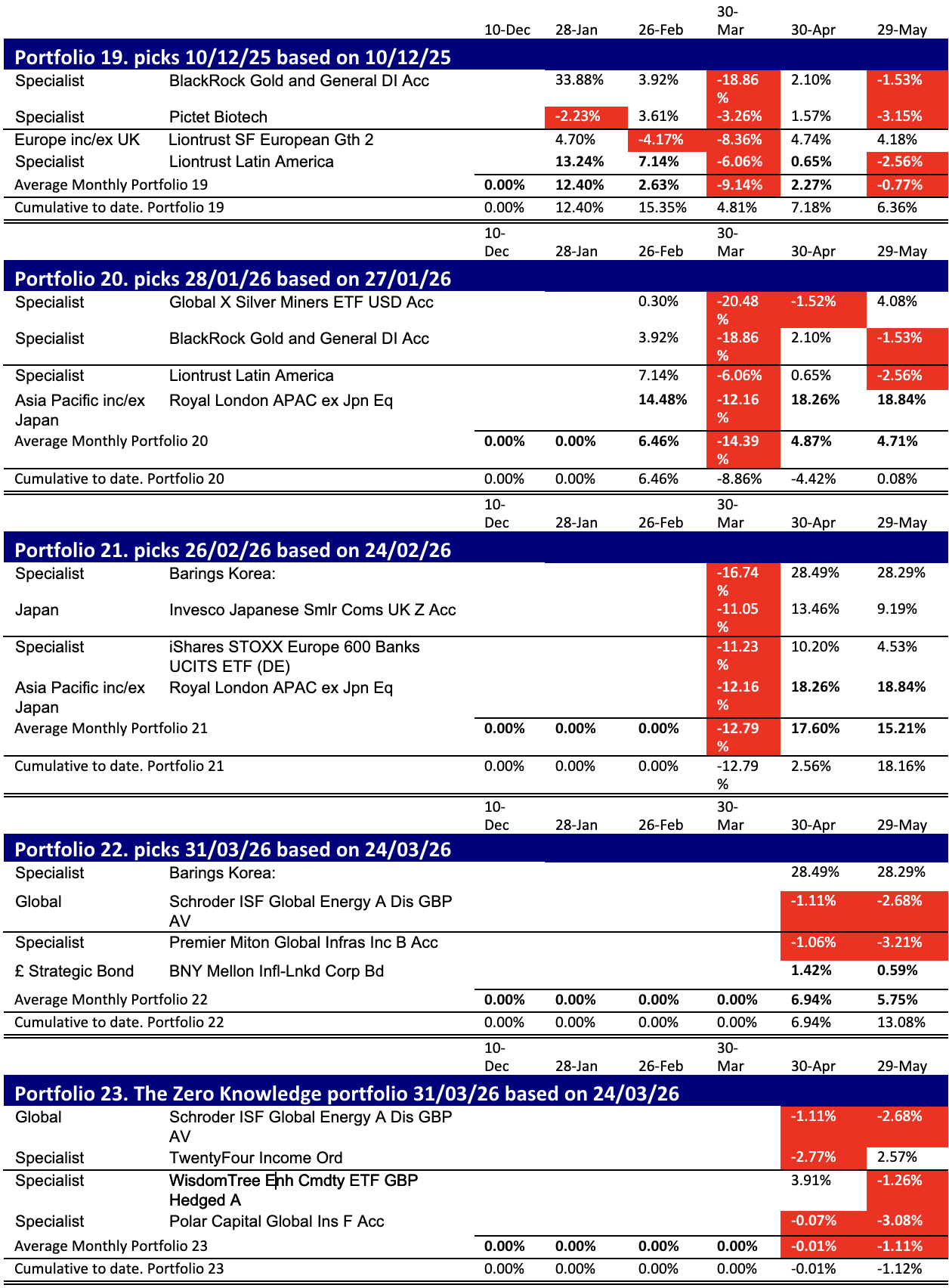

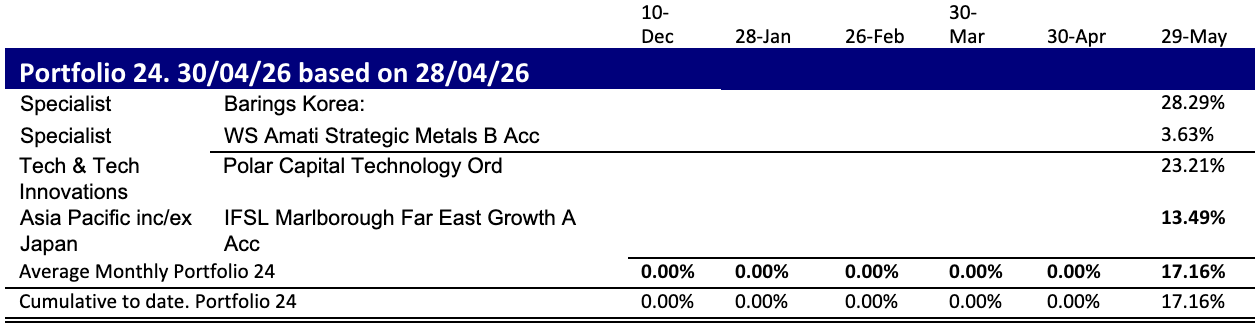

Our portfolios

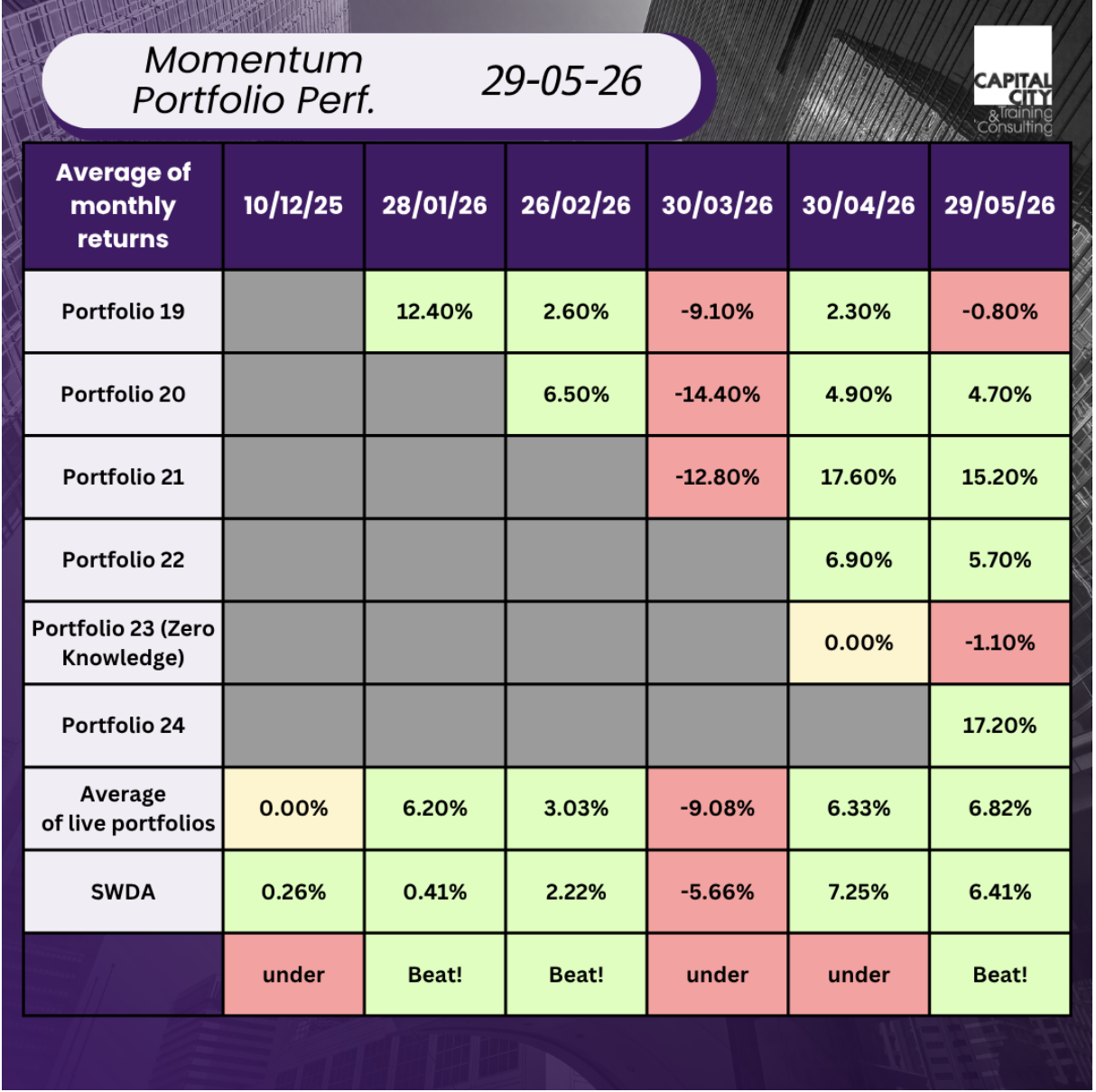

The relative performance If we leave out the “no-knowledge” portfolio is neutral, we’ve beaten or matched SWDA in four out of the last six months. As I have said in many of the previous blogs, our performance critically reflects the relative weights of Technology in our portfolios vs SWDA. Now the market is going crazy for tech again, it’s tech or nothing! SWDA has benefited from a bigger allocation.

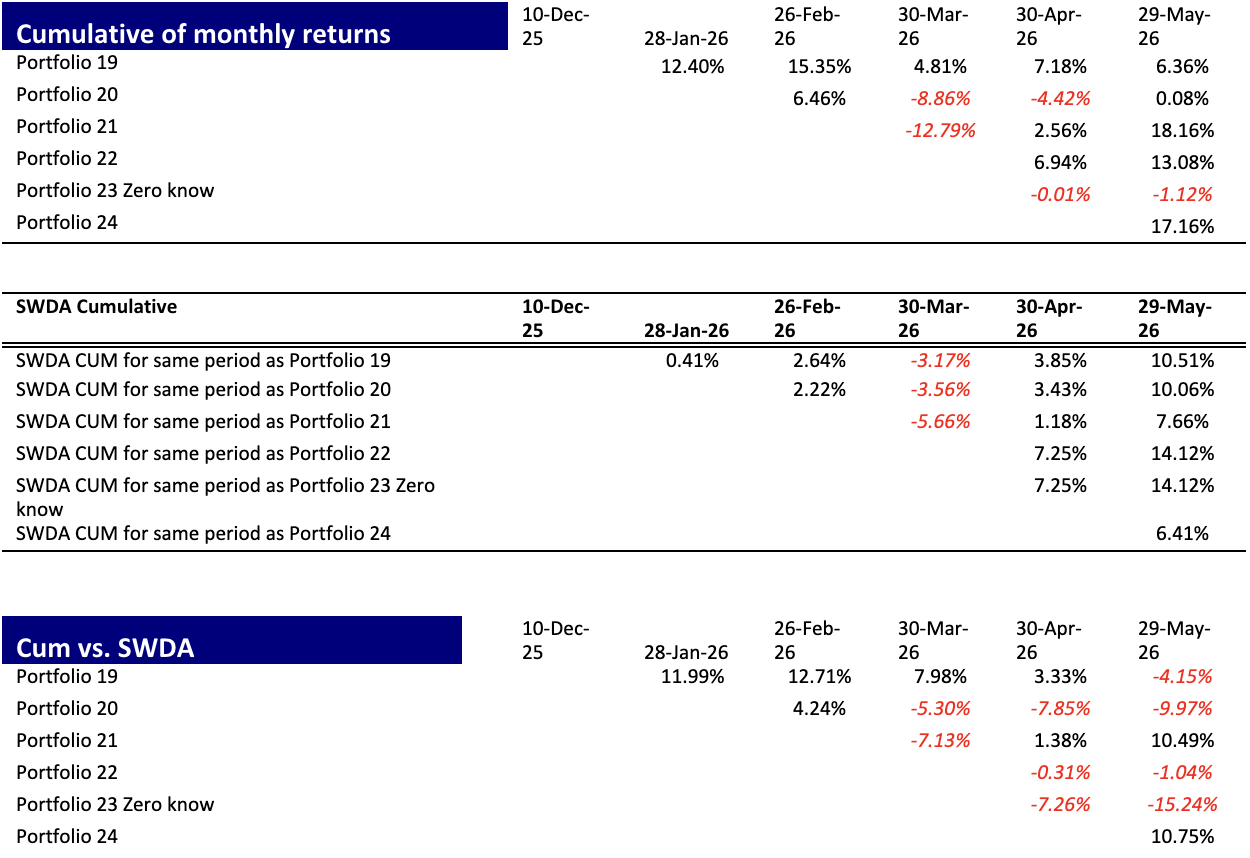

Is there value in the strategy? The following tables shows 1) Cumulative returns of the SWDA Index and 2) the relative Cumulative performance of each fund over the same horizon in each case. As you can see 2 out of 6 portfolios have outperformed on a cumulative basis.

How have the individual portfolios performed?

Momentum in May and a new portfolio Twenty-FIVE

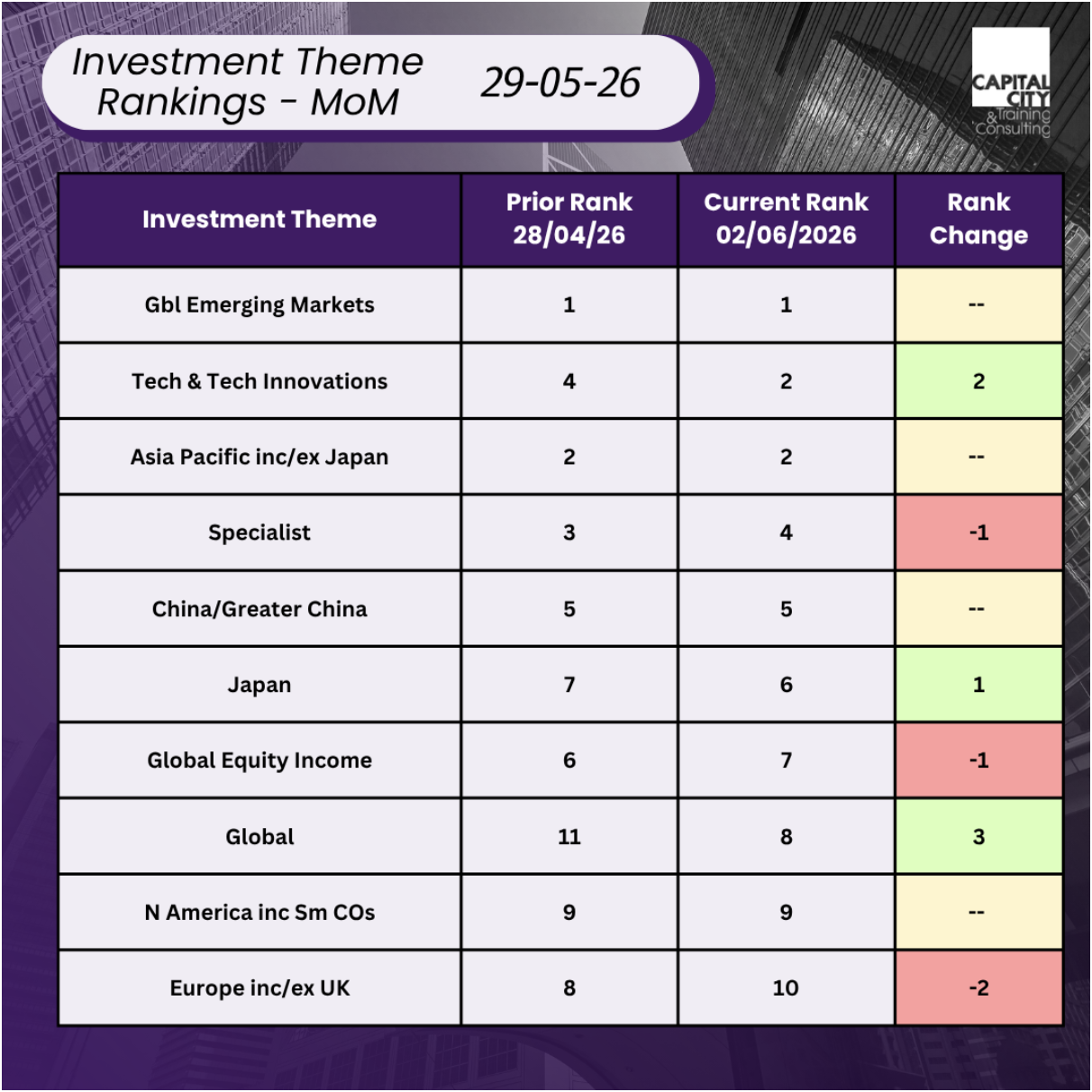

If we look at the momentum over the last four weeks, then the ranking would be:

- Tech

- Global emerging markets

- Asia Pacific inc/ex Japan

- Global funds

If we take the pure momentum approach, allocating as per the 4-week momentum picture is completely consistent with the 6-month momentum picture.

A caveat

I’ve talked about the warning signs above and it’s easy to argue markets appear to be in a state of euphoria. Equally markets can stay irrational longer than you can stay solvent (betting against them). There is a good argument for an investor – rather than a momentum blogger – to take cash off the table and rotate into real assets given where we are in the economic cycle.

However, I am going to stick with the spirit of the experiment and not dilute the momentum bet, as I have once before. High return, high volatility of returns! Let’s see how the market looks after the Space X IPO on 12th June!

This month’s portfolios

find us on substack & Youtube

access the data for yourself

Former banker turned entrepreneur. I successfully restructured, purchased, managed and sold a private engineering group, Steel Line Ltd, through an LBO and was also an equity partner in Corporate Training Group which my partners and I successfully sold to the AIM listed ILX group in 2006. I established Capital City Training Limited in early 2010 with my business partner Greg. We acquired MS Consultants a few years ago (so I’m still doing a bit of M&A). I have had non-exec roles for a small and growing VA/recruitment business and a fast-growing beverage logistics company. I am also an active investor.

Capital City Training is a full service technical and management development training company focused on the banking, wealth management and broader financial services and accounting industries. Having said all that, in the last couple of years we’ve been branching out into training for non-financial companies – manufacturing, retail, tech, defense.. so old and new economy. We also provide consultancy around modelling and are currently working for a leading PPP/PFI advisory firm. We have delivered training in every continent of the world in 2024… except Antarctica. Perhaps in 2025?! Watch this space.

Capital’s dedicated faculty combine extensive line experience as corporate financiers, bankers, traders, portfolio managers and equity analysts together with over 60 years of experience in learning and development as both procurers and providers of tailored in-house training, eLearning and blended learning. Our faculty also includes experienced Management development training specialists allowing us to provide HR consultancy services, management development training and also innovative integrated management development & technical training events. Capital City’s faculty embody over 100 years of line experience across the fields of accounting, corporate finance, derivatives, credit, lending, investment, equity research transaction banking and origination.