Equities vs Bonds: Understanding the Core Differences for Portfolio Construction

Every investor faces the fundamental choice between equities and bonds, yet the decision extends far beyond simple return expectations — it’s about managing risk, timing, and psychological comfort throughout market cycles. Understanding the structural differences between these asset classes is essential for anyone working in wealth management, portfolio construction, or investment banking. This article examines the core distinctions between equities and bonds, exploring how liquidation priority affects investor risk, why bonds serve as a volatility hedge, and how interest rate movements impact each asset class differently.

Article Contents

- The Fundamental Differences: Ownership vs Lending

- Liquidation Priority and Capital Structure

- Returns and Risk: The Long-Term Trade-Off

- Understanding Sequence of Returns Risk

- Bonds as a Volatility Hedge in Portfolio Construction

- Rebalancing and Risk-Adjusted Returns

- Interest Rate Sensitivity: How Rates Affect Each Asset Class

- Common Interview Questions

- FAQs

Key Takeaways

| Key Points | Details |

|---|---|

| Ownership vs Lending | Equities represent ownership in a company with residual claims on profits and assets, while bonds represent lending with contractual claims to fixed interest and principal repayment |

| Position in Capital Structure | In liquidation, bondholders are paid before shareholders. Equity holders often receive nothing in bankruptcy scenarios |

| Risk–Return Trade-Off | Equities offer higher long-term return potential (historically 8–10%) but with higher volatility. Bonds typically offer lower returns (4–6%) but greater stability |

| Income Certainty | Bonds provide predictable coupon payments. Equity dividends are discretionary and may be reduced or suspended during downturns |

| Capital Preservation | Investment grade and government bonds provide stronger capital preservation characteristics than equities, especially during market stress |

| Sequence of Returns Risk | Poor returns early in retirement combined with withdrawals can permanently damage a portfolio. Bonds provide liquidity to avoid selling equities at depressed prices |

| Bonds as Volatility Hedge | High-quality bonds often have low or negative correlation with equities during market stress, reducing overall portfolio drawdowns |

| Rebalancing Advantage | Fixed income allocations allow investors to rebalance by selling bonds and buying equities during downturns, effectively “buying low” |

| Efficient Portfolio Construction | A diversified portfolio (e.g., 60/40 equities/bonds) historically captures much of equity upside with materially lower volatility and drawdowns |

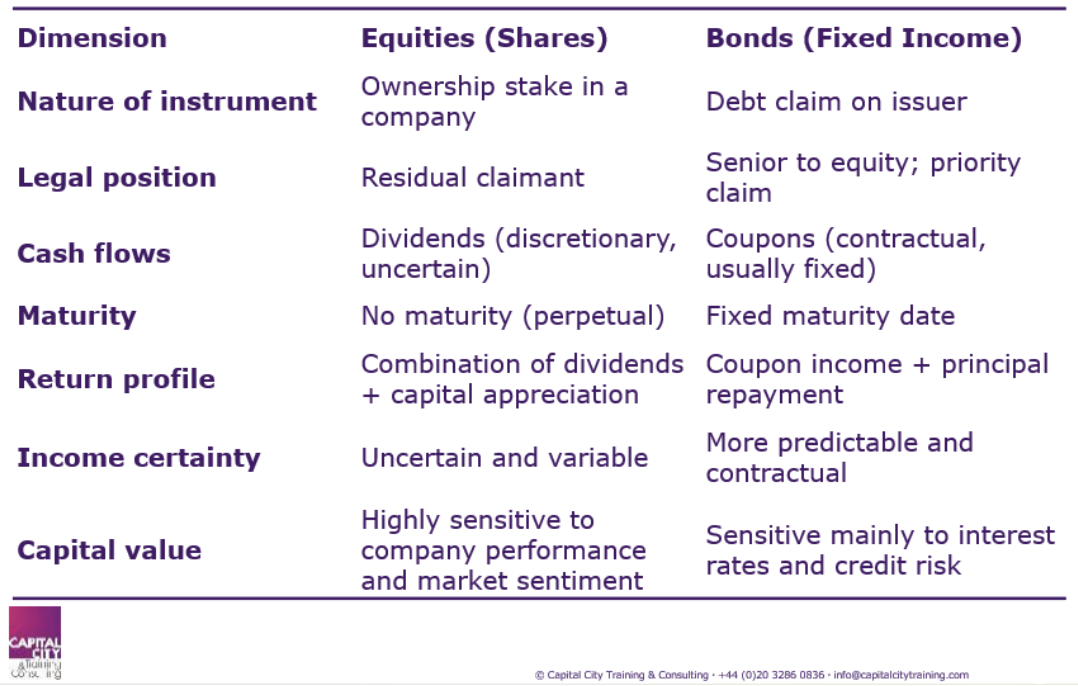

The Fundamental Differences: Ownership vs Lending

When you purchase equity, you acquire ownership in a company. When you buy a bond, you become a creditor. This distinction is not merely semantic — it fundamentally shapes the risk-return profile of each investment and determines your position in the capital structure.

Equity investors hold residual claims on a company’s assets and earnings. After all obligations are met — wages, suppliers, taxes, and crucially, bondholders—shareholders receive what remains. This residual nature means equity returns are theoretically unlimited when companies perform well, but shareholders bear the first losses when performance deteriorates.

Bondholders, conversely, have contractual claims to fixed interest payments and principal repayment at maturity. These obligations are legally enforceable, and failure to meet them constitutes default. The fixed nature of bond returns means upside is capped at the coupon rate plus any capital appreciation from interest rate movements, but this structure provides greater income certainty.

A Quick Comparison of Equities vs Bonds:

Liquidation Priority and Capital Structure

In liquidation scenarios, bondholders’ senior claim on assets versus shareholders’ residual claim becomes starkly apparent. The capital structure operates as a hierarchy: secured creditors are paid first, followed by unsecured bondholders, then preferred shareholders, and finally ordinary shareholders. In practice, equity holders frequently receive nothing in bankruptcy proceedings.

This liquidation priority translates directly to risk profiles. High quality bonds from investment grade issuers carry substantially lower default risk than equity investments in the same companies. Even if a company faces financial distress, bondholders may recover significant portions of their investment, whilst equity investors face total loss.

The implications for income certainty and capital preservation are considerable. Bonds provide predictable cash flows through coupon payments, making them suitable for investors requiring stable income. Equities offer dividends, but these are discretionary and can be suspended during downturns. For capital preservation, bonds—particularly government bonds and investment grade corporate bonds—offer far greater certainty than equities, which can experience severe drawdowns during market stress.

Returns and Risk: The Long-Term Trade-Off

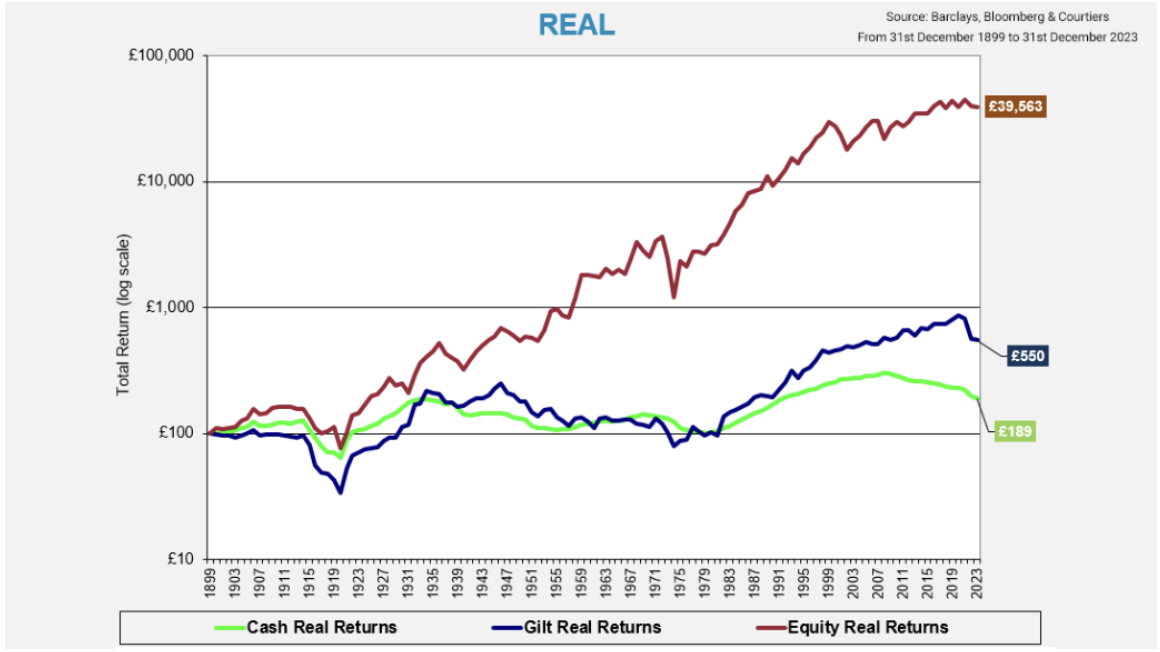

Historical data consistently demonstrates that equities typically outperform bonds over extended periods. This equity premium exists precisely because shareholders accept greater risk. Over multi-decade horizons, equity markets have delivered annualised returns of 8-10% compared to 4-6% for bonds, though these figures vary by market and period.

However, if investing for the long-term, the evidence of investing in equities is clear – shown below. Note that the bond-returns below are UK government bonds (low risk). Corporate bonds will attract a higher return due to additional the credit risk premium commanded by lenders to cover the risk of default.

Real (Inflation-adjusted) purchasing power of £100 invested in December 1899:

Chart source: Courtiers.co.uk Equity and Gilt Study 2024

However, the question “Why should I invest in bonds if stocks grow over time?” misses a critical consideration: sequence of returns risk. Long-term average returns tell only part of the story. The order in which returns occur matters enormously, particularly for investors making withdrawals.

Understanding the Sequence of Returns Risk

Sequence of returns risk represents the danger that poor returns early in your investment or withdrawal period can permanently impair your portfolio’s ability to recover. This timing dimension is why balls of steel investors who can hold through any downturn still benefit from bond allocations.

Consider the double-whammy scenario: you retire and begin drawing income from your portfolio just as equity markets enter a severe bear market. You’re forced to sell shares at depressed prices to fund living expenses, crystallizing losses, and reducing the capital base available for future growth. When markets eventually recover, your portfolio has fewer shares to participate in the upswing. This sequence can devastate long-term outcomes despite strong average returns over the full period.

Bonds provide a cash buffer to avoid selling equities at market lows. When equity markets decline, you draw from your fixed income allocation instead, allowing your equity holdings to recover without forced selling. This approach lets you self-insure against downturn without abandoning equity exposure entirely. You’re not timing the market; you’re managing liquidity needs across market cycles.

The difference between long-term growth and short-term liquidity needs is fundamental to portfolio construction. A 25-year-old accumulating wealth can afford to hold 100% equities because they won’t need the capital for decades. A 65-year-old retiree requiring regular withdrawals cannot accept the same volatility, regardless of equities’ superior long-term returns. The ability to sleep better knowing you won’t be forced to sell in a downturn has genuine financial value, not merely psychological comfort.

Bonds as a Volatility Hedge in Portfolio Construction

Fixed income allocations serve multiple functions beyond capital preservation. Bonds act as a volatility hedge, reducing portfolio drawdowns during equity market stress. This isn’t about eliminating risk—it’s about managing risk-adjusted returns and enabling strategic decision-making during market dislocations.

High quality bonds often exhibit low or negative correlation with equities during market stress. When equity markets sell off sharply, investors typically rotate into government bonds and investment grade corporate bonds, driving bond prices higher even as equity values fall. This negative correlation during downturns—though not guaranteed—provides diversification benefits that reduce overall portfolio volatility.

The mathematical reality is that lower volatility can improve long-term compound returns. A portfolio that falls 50% requires a 100% gain to recover. A portfolio that falls 30% requires only a 43% gain. By reducing the depth of drawdowns, bonds can enhance long-term wealth accumulation even if they underperform equities in isolation.

Rebalancing and Risk-Adjusted Returns

How fixed income allocation enables buying equities during market dips represents one of the free lunch opportunities in investing. When equity markets decline significantly, your portfolio becomes underweight with equities relative to your target allocation. Rebalancing involves selling bonds and buying equities, effectively forcing you to buy low.

This rebalance back mechanism is powerful. During the 2020 market crash, investors with fixed income allocations could purchase equities at substantial discounts, then benefit from the rapid recovery. Those holding 100% equities had no dry powder to deploy and could only watch their portfolios decline.

The concept of diversification benefits and risk-adjusted returns extends beyond simple volatility reduction. A portfolio of 60% equities and 40% bonds has historically delivered more than 60% of the returns of a 100% equity portfolio whilst experiencing substantially smaller drawdowns. This illustrates what we mean by more ‘efficient’ investing – similar or better returns for lower risk exposure. For many investors, this trade-off is attractive—you sacrifice modest returns for significantly improved risk characteristics. It’s the closest thing you’ll get to a ‘free lunch’ in the investment world!

Practical approaches typically involve investment grade bond index funds and systematic asset allocation strategies. Rather than attempting to time markets, you establish a target allocation based on your risk tolerance, time horizon, and liquidity needs, then rebalance periodically. Some investors ladder their cash and bonds, creating a maturity schedule that provides predictable liquidity whilst maintaining exposure to longer-duration bonds for diversification.

The key is not to chase yield by reaching for high-yield bonds or other risky fixed income. High-yield bonds behave more like equities during stress periods, defeating the purpose of bond allocation. Investment grade bonds — government bonds, high-quality corporate bonds, and diversified bond index funds—provide the volatility hedge and rebalancing opportunities that make fixed income valuable.

Interest Rate Sensitivity: How Rates Affect Each Asset Class

Interest rate changes affect equities and bonds through distinct mechanisms, though both asset classes respond to rate movements. Understanding these relationships is essential for portfolio management and risk assessment.

Bonds exhibit direct, inverse relationships with interest rates. When rates rise, existing bonds with lower coupon rates become less attractive, and their prices fall. When rates decline, existing bonds with higher coupons become more valuable, and prices rise. This relationship is quantified through duration — a measure of price sensitivity to interest rate changes. A bond with a duration of 7 years will decline approximately 7% in value for each 1% rise in interest rates. Shifts in the rates to that degree are usually found, but this illustrates how quantifiable risk in bonds actually is – it’s much more scientific than equity risk evaluation.

This interest rate risk is painful to hold during rising rate environments, as bond portfolios experience mark-to-market (value) losses. However, if you hold bonds to maturity, you receive par (redemption) value regardless of interim price fluctuations. Additionally, as bonds mature in a rising rate environment, you can reinvest proceeds at higher yields, eventually benefiting from increased rates.

Equities face indirect interest rate effects through multiple channels. Rising rates increase discount rates applied to future cash flows, reducing the present value of companies’ earnings. Higher rates also increase borrowing costs, potentially compressing profit margins for leveraged companies. Finally, rising rates often signal central bank tightening to combat inflation, which can slow economic growth and reduce corporate earnings.

However, equities are not bonds. Companies can grow earnings, raise prices, and adapt to changing conditions in ways that fixed income securities cannot. Over long periods, equity returns have shown relatively weak correlation with interest rate levels. The equity beta (sensitivity) to interest rates is far lower than bonds’ direct sensitivity.

The relationship becomes more complex when considering why rates are changing. Rates rising due to strong economic growth may support equity valuations despite higher discount rates. Rates rising due to inflation concerns present a more challenging environment for both asset classes. Rates falling due to recession fears may benefit bonds whilst harming equities.

For portfolio construction, this means bonds and equities can provide diversification even though both are affected by interest rates. The mechanisms differ sufficiently that the assets don’t move in lockstep. During the 2022 rate hiking cycle, both equities and bonds declined — a reminder that diversification reduces but doesn’t eliminate risk. However, over full market cycles, the diversification benefits remain robust.

Common Interview Questions

Candidates interviewing for roles in wealth management, portfolio management, or investment banking should expect questions probing their understanding of equities versus bonds. These questions assess both technical knowledge and practical application.

Technical and Conceptual Questions

Explain the relationship between bond prices and interest rates.

Bond prices and interest rates move inversely. When interest rates rise, newly issued bonds offer higher coupons, making existing bonds with lower coupons less attractive. Investors will only purchase these existing bonds at discounted prices that bring their yield to maturity in line with current market rates. The magnitude of price change depends on the bond’s duration—longer-duration bonds experience greater price sensitivity. This relationship is fundamental to fixed income valuation and risk management.

Describe how you would construct a portfolio for a client nearing retirement.

Portfolio construction for a client nearing retirement requires understanding their specific circumstances: time horizon, income needs, risk tolerance, and existing assets. Generally, you would increase fixed income allocation to reduce volatility and provide a cash buffer for withdrawals, avoiding sequence of returns risk. A common approach might be a 40-60% equity allocation with the remainder in high quality bonds and cash. You would ladder bonds to match anticipated withdrawal needs over the first 5-10 years, allowing equity holdings time to recover from potential downturns. The specific allocation depends on the client’s ability to guardrail their spending if markets decline and their psychological comfort with volatility.

What is meant by risk tolerance and how does it inform asset allocation decisions?

Risk tolerance encompasses both the financial capacity to absorb losses and the psychological willingness to endure volatility. Financial capacity depends on time horizon, income stability, and liquidity needs. Psychological tolerance reflects how market downturns affect behaviour—whether you can maintain discipline or panic sell at market lows. Asset allocation should reflect both dimensions. A young professional with stable income and decades until retirement has high financial capacity for risk but may still have low psychological tolerance. Conversely, a wealthy retiree might have high financial capacity but appropriately chooses conservative allocations due to limited time to recover from losses. The goal is finding an asset allocation the client can maintain through full market cycles, as the best theoretical portfolio is worthless if the client abandons it during stress.

Understanding equities versus bonds extends beyond academic knowledge — it requires appreciating how these asset classes function within portfolios across market environments. The choice between equities and bonds is rarely binary. Most investors benefit from holding both, with allocations reflecting their specific circumstances, time horizons, and the often-overlooked reality that managing risk and maintaining discipline matters as much as maximising returns.