Annual Percentage Rate (APR): What it is, How it’s Calculated, and Why Does it Matter

In the UK and US, it is a legal requirement for the APR to be disclosed in the consumer credit market. Therefore, it is the most commonly seen % interest rate seen. APR is often described as the price of money—but in practice, it’s frequently misunderstood, even by those working in financial services. While it’s designed as a consumer protection tool to help compare loans easily, the reality is more nuanced.

APR represents the % total cost of borrowing, including fees and interest and is rate of annualised interest. It differs fundamentally from the nominal interest rate, which only accounts for the cost of borrowing the principal. Fees are the key. Understanding APR is essential for evaluating credit products and advising clients, yet many professionals struggle to explain why APR sometimes feels misleading or why it doesn’t always reflect what borrowers actually pay.

This article clarifies what APR is, how it’s calculated, and where its limitations lie—knowledge that’s crucial whether you’re structuring credit products, advising clients, or preparing for interviews in financial services.

Article Contents

Key Takeaways

| Key Point | Details |

| Definition of APR | APR is the total annualised cost of borrowing, including fees and interest. It’s a standardised metric designed to help consumers compare credit products across lenders. |

| APR Includes Fees | It differs from the nominal interest rate by incorporating mandatory fees. The interest rate is the cost of borrowing the principal alone; APR includes origination fees, closing costs, and other charges. |

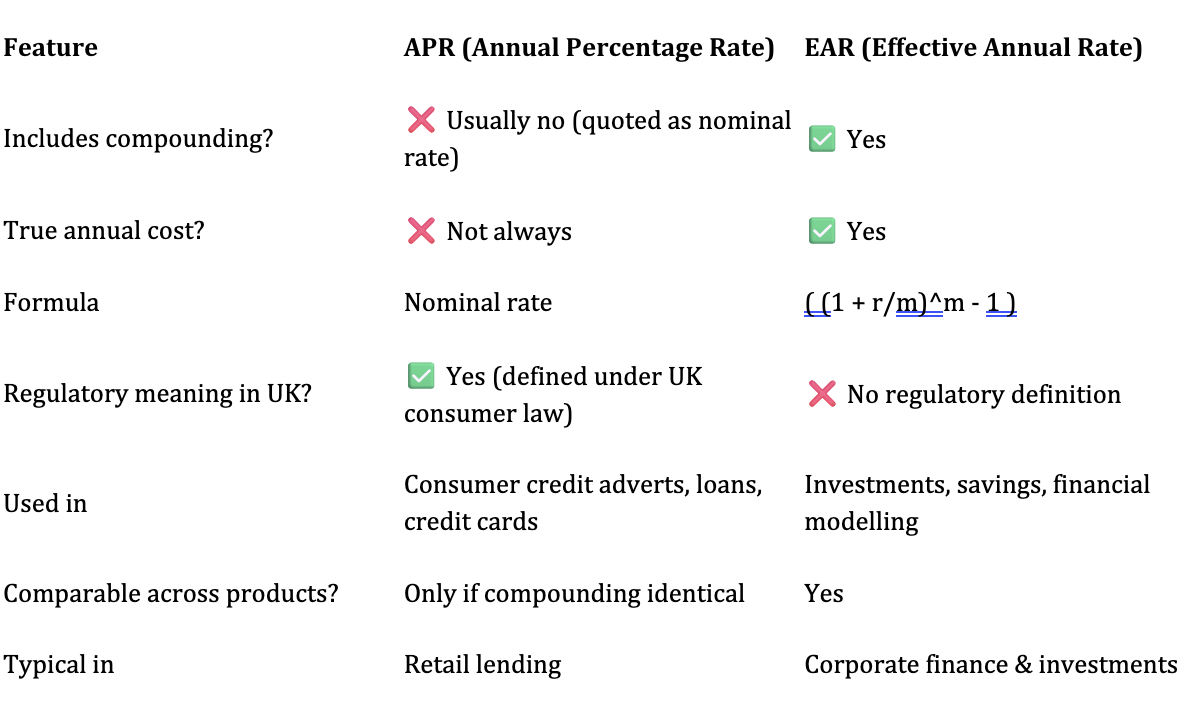

| EAR Shows Compounding | APR is not a true compound rate, EAR is – showing the compound annualised rate of interest. It is the same as an internal rate of return (IRR) on the pattern of cashflows. Easily computed in Excel. |

| EAR Shows True Cost | APR is a comparison tool, not a measure of effective interest—that’s EAR. APR doesn’t account for compounding, so it understates the true cost of products with frequent compounding. EAR provides a more accurate picture of what you’ll actually pay. |

| Variable APR | Variable APR can change based on benchmark rates or borrower behaviour. If you have a variable-rate product, your APR will fluctuate with changes in the base rate. Lenders may also adjust your APR based on your credit score or payment history. |

| APR’s Limitations | Understanding APR’s limitations is as important as knowing how to calculate it. APR assumes you’ll hold the loan to term, make all payments on time, and never pay early. In practice, these assumptions often don’t hold, which is why APR sometimes feels misleading. It’s a useful tool, but not the final word on cost. |

What Is APR and Why Does It Exist?

APR, or Annual Percentage Rate, is a standardised measure of the cost of borrowing expressed as an annual percentage. It was introduced as a consumer protection mechanism under the Truth in Lending Act in the United States (with similar regulations in the UK and elsewhere) to ensure transparency in lending.

Before APR became mandatory, lenders could advertise interest rates without disclosing additional fees, making it nearly impossible for consumers to compare products. They could also quote periodic rates – e.g. “1% pcm”, or “3.5% quarterly” or “14% pa” which makes it difficult for borrowers to make quick decisions on the back of comparable rates. Similarly, one lender might offer a 5% interest rate with £500 in fees, while another offered 6% with no fees. Without a standardised metric, borrowers couldn’t easily determine which was cheaper.

APR solves this by rolling interest and mandatory fees into a single annualised figure. This allows consumers to compare loans easily across lenders, at least in theory.

APR as a Standardised Comparison Tool

The primary purpose of APR is comparison. By law, lenders must disclose APR on credit cards, mortgages, personal loans, and other credit products. This creates a level playing field where borrowers can evaluate offers side by side.

APR includes both interest and mandatory fees in a single percentage. These fees might include origination fees, broker fees, closing costs, and other charges required to obtain the loan. Voluntary fees—such as payment protection insurance or optional account features—are excluded.

The problem is that APR doesn’t always reflect the effective interest you’ll actually pay. It assumes you’ll hold the loan to full term, make all payments on schedule, and never pay early. In practice, borrowers often refinance, pay off loans early, or miss payments—all of which change the actual cost. This is why some people say APR feels misleading or question whether it’s actually useful.

APR is better than nothing, but it’s not perfect. It’s a starting point for comparison, not the final word on cost.

How APR Differs from the Nominal Interest Rate

One of the most common sources of confusion in financial services is the distinction between APR and the nominal interest rate. Clients often use the terms interchangeably, but they represent different things.

The interest rate is the cost of borrowing the principal alone. If you borrow £10,000 at a 12% interest rate, you’ll pay £1,200 in interest over one year (assuming simple interest). The interest rate doesn’t account for any other costs associated with obtaining the loan.

APR, by contrast, includes origination fees, broker fees, closing costs, and other mandatory charges. If that same £10,000 loan has a £200 origination fee, the APR will be higher than 5% because the total cost of borrowing is now £1400, not £1200.

What’s Included in APR vs Interest Rate

Interest rate is the cost of borrowing the principal alone. It’s the percentage charged on the outstanding balance, typically expressed as an annual rate. This is the figure lenders use to calculate your monthly payment.

APR includes origination fees, broker fees, closing costs, and other mandatory charges. These are one-time or recurring costs that you must pay to access the credit. For example, a mortgage might have a 4% interest rate but a 4.2% APR once you factor in valuation fees, arrangement fees, and legal costs.

In practice, this means APR is always equal to or higher than the stated interest rate. If a lender advertises an APR that’s identical to the interest rate, it means there are no additional fees—or the fees are so small they don’t materially affect the calculation.

This distinction matters when advising clients. A loan with a lower interest rate but high fees might have a higher APR than a loan with a higher interest rate and no fees. The APR gives you a clearer picture of the total cost, but only if the borrower holds the loan to term.

How APR Is Calculated

APR is calculated by annualising the total cost of borrowing, including both interest and fees, and expressing it as a percentage of the principal. The formula is straightforward, but the inputs vary depending on the product.

Formula to Calculate APR

The basic formula for APR is:

APR = [(Fees + Interest) / Principal] / Number of Days in Loan Term × 365 × 100

This formula assumes the loan runs to full term without early repayment. If you pay off a loan early, the APR calculation becomes less accurate because the fees are spread over fewer days, effectively increasing the annualised cost.

Different products—credit cards, mortgages, car loans—may include different fee structures. A mortgage APR might include valuation fees, arrangement fees, and legal costs. A credit card APR typically includes annual fees but not transaction fees (since those are optional). A car loan APR might include documentation fees and dealer charges.

The calculation also assumes regular, on-time payments. If you miss payments or incur late fees, those aren’t reflected in the advertised APR, though they will increase your actual cost.

Compounding Frequency: Daily vs Monthly

APR itself is an annualised figure, but interest may compound daily, monthly, or annually. This is where confusion arises. People often ask, is this APR compounded daily or monthly? The question reflects real confusion—APR doesn’t compound, interest does.

APR is a way of expressing the cost of borrowing over a year. The compounding frequency determines how often interest is calculated and added to the balance. For example, a credit card might have an APR of 18%, but if interest compounds daily, the effective cost will be slightly higher than 18% because you’re paying interest on interest.

EAR

This is where Effective Annual Rate (EAR) becomes relevant for comparing actual cost. EAR accounts for compounding, while APR does not. If you’re evaluating two products with the same APR but different compounding frequencies, the one with more frequent compounding will have a higher EAR—and a higher actual cost.

APR vs Effective Annual Rate (EAR)

APR and EAR are often confused, but they measure different things. APR is a standardised comparison tool. EAR is a measure of the true cost of borrowing, accounting for compounding.

The formula for EAR is:

EAR = (1 + r/n)^n – 1

Where r is the nominal interest rate and n is the number of compounding periods per year.

For example, if a credit card has an APR of 18% compounded monthly, the EAR is approximately 19.56%. This means the actual cost of borrowing is higher than the advertised APR because interest is calculated and added to the balance 12 times per year.

A Comparison of APR and EAR

Why EAR Matters More for Actual Cost

EAR accounts for compounding, APR does not. This makes EAR a more accurate measure of what you’ll actually pay, especially for products with frequent compounding.

For products with frequent compounding—such as daily on credit cards—EAR will be higher than APR. The difference can be significant. A credit card with an 18% APR compounded daily has an EAR of approximately 19.72%, nearly two percentage points higher.

In practice, APR is better for comparing products; EAR is better for understanding true cost. When you’re evaluating loan offers, APR gives you a quick way to compare. When you’re calculating the actual interest you’ll pay, EAR is more ‘complete’. Having said that, most people pay off their credit card interest each month, so they do not pay a full year of compounding, only one month.

This distinction is important in client conversations. If a client asks why their credit card balance is growing faster than the APR suggests, the answer is compounding. The APR doesn’t capture the effect of interest on interest, but EAR does.

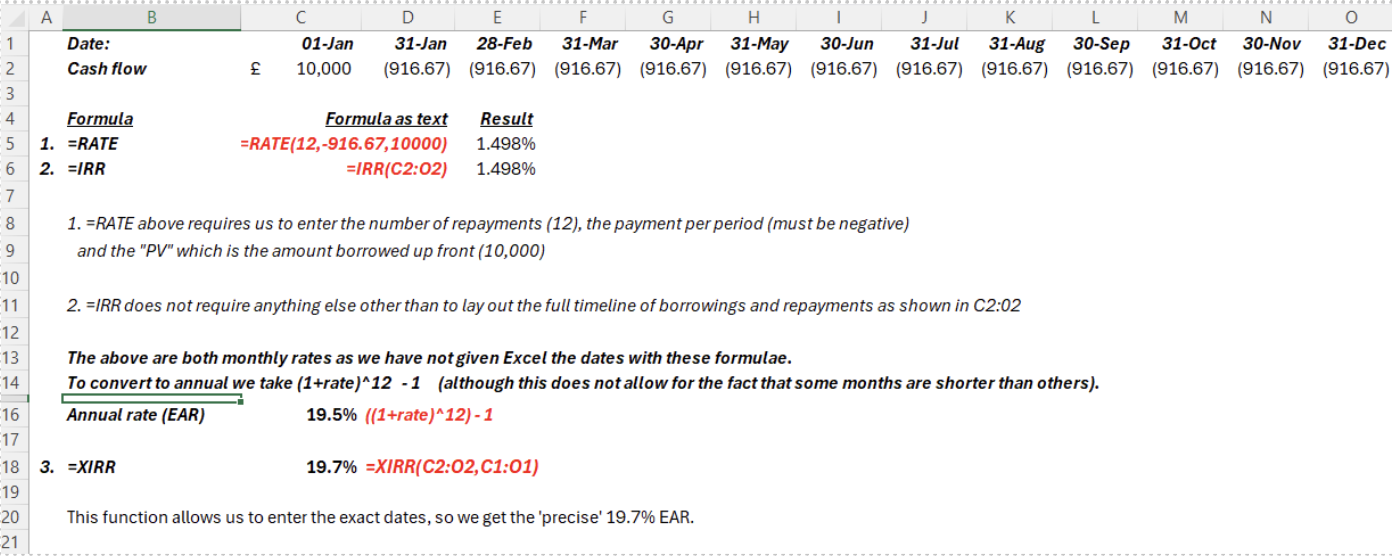

Example of EAR computation on a loan in Excel:

Sometimes you may be working out EARs based on a pattern of repayments on a loan. This requires a bit of help from Excel. Here’s an example:

Let’s say you borrow £10,000 on Jan 1. You will repay £916.67 each month for 12 months.

So total borrowed: £10,000

Total repaid: £916.67 x 12 = £11,000.

You would look at this and say interest paid is £1000. Although that is true, the interest rate is NOT 10% (1,000/10,000). Why? You start repaying the loan after 1 month but continue to pay £916.67 per month even though your principal borrowing is reduced. The EAR gives you a clear picture of the true (effective) rate. In Excel we can use the RATE function, or the IRR and XIRR function.

Variable APR and How It Changes Over Time

Not all APRs are fixed. Many credit products—particularly credit cards and variable-rate mortgages—have APRs that change over time. Understanding what drives these changes is essential for advising clients and managing your own borrowing.

A variable APR is tied to a benchmark rate, such as the Bank of England base rate or, historically, LIBOR. When the benchmark rate rises, so does the APR. When it falls, the APR should fall as well, though lenders don’t always pass on decreases as quickly as they implement increases.

Common Interview Questions on APR

APR is a common topic in interviews for roles in retail banking, credit analysis, and financial advisory. Interviewers use it to assess both technical knowledge and the ability to communicate complex concepts clearly.

Typical Questions and How to Answer Them

-

- “Why do lenders advertise APR rather than interest rate?”

Answer: Regulatory requirement and consumer protection. Lenders are legally required to disclose APR under the Truth in Lending Act and similar regulations. APR provides a standardised way to compare products, making it harder for lenders to obscure costs with hidden fees. It’s not perfect, but it’s better than allowing lenders to advertise only the interest rate. - “How would you explain APR to a client who thinks it’s misleading?”

Answer: Acknowledge the limitations, then clarify what it does and doesn’t show. You might say: “APR is designed to help you compare loans, but it assumes you’ll hold the loan to full term and make all payments on time. If you pay off the loan early, the actual cost might be different. It’s a useful starting point, but not the whole picture.” - “Why do car dealers emphasise APR in commercials?”

Answer: HIt’s a legal requirement and a competitive differentiator as it includes fees, though it can be used to obscure other costs. Dealers must disclose APR in advertising, and a low APR is an attractive selling point. However, dealers sometimes use low APR offers to distract from high vehicle prices or unfavourable trade-in values. The APR might be competitive, but the overall deal might not be.

- “Why do lenders advertise APR rather than interest rate?”

An experienced finance and training professional and Co-Founder of Capital City Training Ltd, Greg has a demonstrated history of working in the financial services sector and has a passion for sharing his knowledge and skills throughout the financial services sector. He has been partnering financial and corporate clients in designing and delivering applied financial programs that make an impact on business outcomes. Greg is skilled in accounting & financial analysis, derivatives and risk management, financial modelling, business valuation and corporate finance and has worked with the worlds leading financial institutions. A strong business development professional and a qualified accountant (ICAEW member), CFA Charterholder and Associate Member of the Association of Corporate Treasurers in the UK (ACT).