ETFs vs Mutual Funds: Which Investment Vehicle Suits Your Strategy?

Both ETFs and mutual funds offer diversified exposure to markets, but their structural differences create distinct advantages for different types of investors. Understanding these distinctions is essential for anyone working in wealth management, fund administration, or investment advisory roles. The choice between these vehicles affects cost structures, tax efficiency, trading flexibility, and operational convenience—factors that directly impact client outcomes and portfolio performance.

This article examines the core structural differences between ETFs and mutual funds, compares their cost considerations including expense ratios and trading commissions, analyses tax efficiency and capital gains distributions, and explores the practical implications for portfolio management. Whether you’re advising clients or managing your own investments, these distinctions matter.

Article Contents

- Structural Differences: Trading Mechanisms and Pricing

- Cost Structures: Expense Ratios and Trading Costs

- Tax Efficiency: Capital Gains Distributions and Tax Drag

- Practical Investment Considerations: Automation and Accessibility

- Common Interview Questions

- Key Considerations for Investment Professionals

Key Takeaways

| Key Points | Details |

|---|---|

| Both Vehicles Provide Diversification | ETFs and mutual funds both offer diversified exposure to markets and asset classes, serving as core portfolio building blocks. |

| Trading Structure Differs Fundamentally | ETFs trade intraday on exchanges at market prices, while mutual funds transact once daily at net asset value (NAV). |

| Execution Control vs Discipline | ETFs allow precise trade timing and pricing, while mutual funds reduce market‑timing risk through end‑of‑day pricing. |

| Expense Ratios Often Favour ETFs | ETFs typically have lower ongoing management fees than comparable mutual funds, especially for passive index strategies. |

| Trading Costs Can Offset Fee Savings | Broker commissions and bid‑ask spreads can erode ETFs’ cost advantage, particularly for small or frequent investments. |

| Mutual Funds Excel at Automation | Mutual funds support automatic investing, systematic contributions, and frictionless dollar‑cost averaging. |

| Tax Efficiency Depends on Account Type | ETFs are more tax‑efficient in taxable accounts, but this advantage disappears in tax‑advantaged accounts like ISAs and SIPPs. |

| No Vehicle Is Universally Better | The optimal choice depends on investor behaviour, contribution pattern, tax status, and the need for flexibility or automation. |

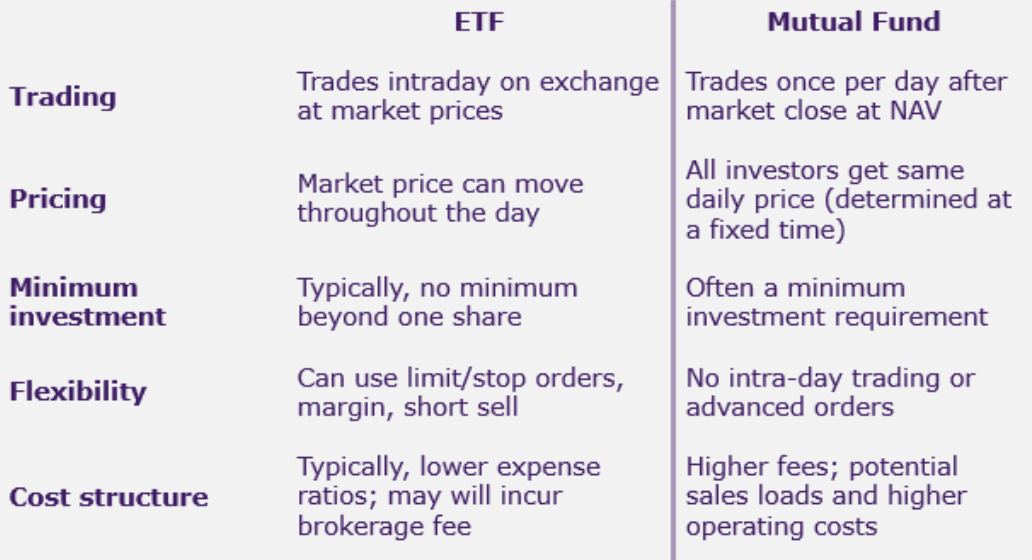

Structural Differences: Trading Mechanisms and Pricing

With both ETS and mutual funds, investors gain access to a diversified portfolio of stocks (or derivatives of them). These may be broad market portfolios, themed portfolios (sustainable, energy, large cap, sovereign bonds, corporate bonds, and so on!) But the way the products are accessed is different – and a ‘need to know’.

The fundamental difference between ETFs and mutual funds lies in how they trade and price their shares. This structural distinction cascades into numerous practical implications for investors and advisers alike.

Overview Comparison

ETFs vs Mutual Fund

How Each Vehicle Trades

ETFs trade throughout the day on exchanges, just like individual stocks. When you purchase an ETF, you’re executing a transaction at the current market price, which fluctuates continuously during trading hours. “Authorised Participants” keep the prices in line with the underlying portfolio and the share in the ETF trades with a bid/ask spread—the difference between the buying and selling price. the buying and selling price.

This spread represents a transaction cost that varies based on the ETF’s liquidity and trading volume – exactly the same as the bid-ask spread on single company shares. For highly liquid ETFs tracking major indices, spreads are typically narrow, often just a few pence. For more specialised or thinly traded ETFs, spreads can be wider, adding to your cost of entry and exit.

This intraday trading capability gives investors precise control over execution. You can place market orders for immediate execution at the prevailing price, or limit orders that only execute when the price reaches your specified level. This flexibility appeals to investors who want to respond to market movements or implement specific timing strategies.

Mutual funds operate entirely differently. They execute all transactions once daily at the based on a once-a-day pricing time. Each day the net asset value (NAV) is determined (a ‘marking to market’ of the portfolio components and this is what determines the price paid / received. When you submit a purchase or redemption order for a mutual fund, it doesn’t matter whether you place it 5 hours before the pricing point or 1 hour before —you’ll receive the same NAV-based price. There’s no bid/ask spread because you’re not trading on an exchange; you’re transacting directly with the fund company at the calculated NAV.

This single pricing point eliminates the possibility of market timing within a trading day. You cannot react to intraday price movements, which some view as a disadvantage but others see as protection against emotional investing. The structure inherently discourages frequent trading and short-term speculation.

Cost Structures: Expense Ratios and Trading Costs

Cost considerations extend beyond the headline expense ratio. A comprehensive analysis requires examining the total cost of ownership, which includes management fees, trading costs, and the impact of investment patterns.

Understanding Total Cost of Ownership

ETFs generally have lower expense ratios than comparable mutual funds, particularly when comparing passive index funds. A typical S&P 500 ETF might charge 0.03% to 0.10% annually, whilst a mutual fund tracking the same index often charges 0.10% to 0.50% or more. This difference compounds significantly over time. On a £100,000 investment, the difference between a 0.05% ETF and a 0.20% mutual fund amounts to £150 annually—£1,500 over a decade before considering compound effects.

However, ETFs incur trading commissions each time you buy or sell, unless your brokerage offers commission-free ETF trading. Even with commission-free trading, the bid/ask spread represents a real cost. For investors making regular contributions—say, monthly investments of £500—these transaction costs accumulate. If the spread costs 0.05% per trade and you invest monthly, you’re paying £0.25 per transaction, or £3 annually on that £500 monthly investment. This seems trivial, but it erodes the expense ratio advantage, particularly for smaller, frequent investments.

Retail investors will pay a lot more than £0.25 per transaction in broker fees too, maybe £7-10 – so if investing a regular monthly amount of, say, £100 then this represents a 7-10% cost! This certainly makes it inefficient trading.

However, mutual funds typically offer commission-free automatic investing through systematic investment plans. You can set up automatic monthly transfers from your bank account, and the fund company executes these purchases without transaction fees. Dividend reinvestment also occurs automatically and without cost. This set it and forget it approach eliminates trading costs entirely for regular investors, making mutual funds more cost-effective for those implementing dollar-cost averaging strategies with smaller amounts.

The crossover point depends on investment size and frequency. For large, infrequent investments, ETFs’ lower expense ratios typically win. For small, frequent investments, mutual funds’ zero-transaction-cost structure often proves more economical, even with higher expense ratios.

Tax Efficiency: Capital Gains Distributions and Tax Drag

Tax efficiency represents one of the most significant structural advantages of ETFs, though its importance varies based on account type and individual circumstances.

The In-Kind Redemption Advantage

ETFs employ a unique creation and redemption mechanism that provides substantial tax advantages. When investors want to redeem ETF shares, authorised participants (typically large financial institutions) can exchange ETF shares for the underlying securities in-kind rather than selling those securities for cash. This in-kind redemption allows the ETF to transfer out shares with the lowest cost basis, effectively purging embedded capital gains from the fund without triggering taxable events.

Mutual funds lack this mechanism. When investors redeem mutual fund shares, the fund must sell underlying securities to raise cash. If those securities have appreciated, the fund realises capital gains, which must be distributed to all remaining shareholders—even those who didn’t redeem shares. This creates tax drag for long-term holders who may face unexpected tax bills from other investors’ redemption activity.

The practical impact is substantial. In a given year, a mutual fund might distribute 2% to 5% of its value as capital gains, forcing investors to pay tax on gains they didn’t actually realise through their own selling. An ETF tracking the same index might distribute nothing. Over decades, this difference compounds significantly, particularly for investors in higher tax brackets.

However, context matters enormously. In tax-advantaged accounts like ISAs or SIPPs in the UK, this advantage disappears entirely. Capital gains distributions don’t create tax liability within these accounts, so the ETF’s structural advantage provides no benefit. For investors holding funds exclusively in tax-advantaged accounts, tax efficiency shouldn’t influence the ETF versus mutual fund decision.

In taxable accounts, the advantage is real and measurable. Tax efficiency becomes particularly valuable during market downturns when mutual funds may be forced to sell appreciated positions to meet redemptions, distributing gains to remaining shareholders even as the fund’s value declines—a particularly frustrating outcome for long-term investors.

Practical Investment Considerations: Automation and Accessibility

Beyond costs and taxes, operational characteristics significantly affect the investor experience and the ease of implementing disciplined investment strategies.

Systematic Investment Plans and Dollar-Cost Averaging

Mutual funds excel at facilitating robotic investment plans. You can establish a systematic investment plan that automatically transfers a fixed amount from your bank account monthly, purchasing mutual fund shares without any action on your part. Because mutual funds allow fractional shares, your entire contribution purchases fund shares—if you invest £500 and the NAV is £47.32, you receive 10.567 shares. Nothing sits uninvested.

This fractional share capability ensures precise investment amounts and complete capital deployment. It’s particularly valuable for dividend reinvestment, where odd dividend amounts automatically purchase additional fractional shares, compounding your returns without leaving cash idle.

ETFs traditionally required purchasing whole shares, creating a practical barrier to complete capital deployment. If you have £500 to invest and the ETF trades at £47, you can only purchase 10 shares, leaving £30 uninvested. For smaller accounts or regular contributions, this cash drag reduces returns over time. Some brokerages now offer fractional ETF shares, narrowing this gap, but availability varies by platform and specific ETF.

The automation difference matters for behavioural reasons beyond mere convenience. Systematic investment plans enforce discipline, removing the temptation to time the market or skip contributions during volatile periods. This peace of mind supports long-term wealth accumulation by eliminating decision fatigue and emotional investing. The set it and forget it approach aligns perfectly with evidence-based investment principles.

ETFs offer advantages in brokerage portability. Because they trade on exchanges, you can hold the same ETF across multiple brokerage accounts or transfer positions between brokers without triggering taxable events. Mutual funds often require an exchange process when moving between platforms, potentially forcing you to sell and repurchase, which may trigger capital gains and disrupt your investment timeline.

For investors who value trading flexibility—perhaps to implement tax-loss harvesting, rebalance tactically, or respond to changing market conditions—ETFs’ intraday liquidity provides clear advantages. You can execute trades immediately at known prices, rather than waiting for end-of-day NAV calculations. This matters less for long-term passive investors but significantly more for those implementing active strategies or managing around specific tax events.

Common Interview Questions

Financial services interviews frequently probe candidates’ understanding of investment vehicles, particularly the nuanced trade-offs between ETFs and mutual funds. These questions assess both technical knowledge and practical judgement.

Technical Knowledge Assessment

Why are ETFs generally more tax-efficient than mutual funds in taxable accounts?

The answer centres on the in-kind redemption mechanism. ETFs can transfer securities to authorised participants without selling them, avoiding capital gains realisation. This allows ETFs to purge low-cost-basis shares from the portfolio without triggering taxable distributions. Mutual funds must sell securities to meet redemptions, realising gains that are distributed to all shareholders. This structural difference means ETF investors control when they realise gains through their own selling decisions, whilst mutual fund investors may face unexpected capital gains distributions from other investors’ redemption activity. The advantage disappears in tax-advantaged accounts where capital gains aren’t taxed.

What are the trade-offs between intraday liquidity and automatic investment capabilities?

Intraday liquidity allows investors to execute trades at specific prices and respond to market movements, providing control and flexibility. However, this same flexibility can encourage market timing and emotional decision-making, which typically harm long-term returns. Automatic investment capabilities remove this temptation, enforcing discipline through systematic contributions regardless of market conditions. The trade-off reflects a tension between control and automation—sophisticated investors may value the former, whilst behavioural evidence suggests most investors benefit from the latter. The optimal choice depends on the investor’s discipline, investment approach, and whether they’re implementing passive or active strategies.

How would you advise a client choosing between an ETF and mutual fund tracking the same index?

The recommendation depends on several factors. First, account type: in tax-advantaged accounts, tax efficiency is irrelevant, so focus on costs and convenience. Second, investment pattern: for large, infrequent investments, ETFs’ lower expense ratios typically win; for small, regular contributions, mutual funds’ zero-transaction-cost automatic investing often proves more economical. Third, investor behaviour: clients prone to emotional investing may benefit from mutual funds’ end-of-day pricing and automatic investment features, which discourage market timing. Fourth, total cost analysis: compare the ETF’s expense ratio plus estimated trading costs against the mutual fund’s expense ratio. Finally, consider the specific funds: some mutual funds offer institutional share classes with expense ratios competitive with ETFs, whilst some ETFs have wide bid/ask spreads that erode their cost advantage. The answer requires understanding the client’s circumstances, not applying a universal rule.

Key Considerations for Investment Professionals

The ETF versus mutual fund decision isn’t binary. Both vehicles serve important roles in portfolio construction, and the optimal choice varies by investor circumstances, account type, and investment approach.

ETFs trade like stocks with intraday pricing and bid/ask spreads, whilst mutual funds execute once daily at NAV. This structural difference affects execution control, trading costs, and the potential for emotional investing. ETFs typically offer lower expense ratios, particularly for passive index funds, but incur trading costs through commissions and spreads. Mutual funds facilitate automatic investing with systematic investment plans and fractional shares, eliminating transaction costs for regular contributors.

Tax efficiency represents a significant ETF advantage in taxable accounts, where in-kind redemptions avoid capital gains distributions that burden mutual fund investors. However, this advantage disappears entirely in tax-advantaged accounts like ISAs and SIPPs, where capital gains aren’t taxed regardless of vehicle.

Mutual funds excel at supporting disciplined, systematic investment approaches through automatic contributions and complete capital deployment via fractional shares. ETFs offer greater trading flexibility and brokerage portability, valuable for investors implementing active strategies or managing around specific tax events.

For financial professionals, the key is matching vehicle characteristics to client needs. Long-term passive investors making regular contributions in tax-advantaged accounts often benefit from mutual funds’ automation and zero-transaction costs. Investors in taxable accounts with larger, less frequent contributions typically favour ETFs’ tax efficiency and lower expense ratios. Neither vehicle is universally superior—the optimal choice emerges from understanding structural differences and aligning them with specific investment circumstances.

An experienced finance and training professional and Co-Founder of Capital City Training Ltd, Greg has a demonstrated history of working in the financial services sector and has a passion for sharing his knowledge and skills throughout the financial services sector. He has been partnering financial and corporate clients in designing and delivering applied financial programs that make an impact on business outcomes. Greg is skilled in accounting & financial analysis, derivatives and risk management, financial modelling, business valuation and corporate finance and has worked with the worlds leading financial institutions. A strong business development professional and a qualified accountant (ICAEW member), CFA Charterholder and Associate Member of the Association of Corporate Treasurers in the UK (ACT).