Asset Allocation for Beginners: A Practical Guide to Building Your First Portfolio

Asset allocation is how you control risk in your investment portfolio—not by predicting markets, but by deciding how much of your money goes into asset classes with different risk / return profiles. For those just starting out, understanding this concept is more important than chasing the highest returns or trying to time market movements.

Asset allocation determines your portfolio’s risk profile and long-term returns. A portfolio heavily weighted towards equities will experience greater volatility but potentially higher growth, whilst one with substantial bond holdings will show more stability but typically lower returns. For beginners, simplicity and consistency matter more than complexity. The most sophisticated allocation model means nothing if you abandon it during the first market downturn.

Understanding your ability to sleep at night during market volatility is crucial. This isn’t merely about theoretical risk tolerance questionnaires—it’s about knowing whether you can hold your investments when they’re down 20% without panicking. Many investors discover their true risk tolerance only when markets turn against them, which is precisely when poor decisions get made.

Article Contents

Key Takeaways

| Key Points | Details |

|---|---|

| Asset Allocation Drives Outcomes | Asset allocation is the primary driver of portfolio risk and long-term returns. It matters more than market timing or individual investment selection. |

| Risk Control, Not Risk Elimination | Diversification across equities, bonds, and cash smooths volatility but does not remove risk. The goal is controlling risk to a tolerable level, not avoiding it entirely. |

| Equities vs Bonds Behaviour | Equities offer higher long-term growth potential but with significant volatility. Bonds provide income, stability, and often act as a shock absorber during equity market downturns. |

| Volatility Tolerance Matters | The right allocation depends on an investor’s ability to stay invested during drawdowns. Portfolios fail when investors abandon them at the worst moments. |

| Risk Capacity vs Risk Tolerance | Financial ability to absorb losses (risk capacity) is distinct from emotional comfort with volatility (risk tolerance). Both must be considered together. |

| Time Horizon Is Critical | Money needed within five years should not be heavily invested in equities. Long time horizons allow portfolios to ride out market cycles safely. |

| Simplicity Beats Complexity | Simple, diversified strategies using low-cost index funds consistently outperform complex approaches for most investors. Complexity increases behavioural risk. |

| Rebalancing Adds Discipline | Regular rebalancing maintains the intended risk profile and enforces systematic “sell high, buy low” behaviour without forecasting markets. |

| Behaviour Is the Biggest Risk | The largest threat to returns is panic-selling, mistiming markets, or abandoning an allocation during downturns—not choosing a slightly imperfect allocation. |

| Portfolio Discipline Wins | Long-term success comes from consistency, disciplined saving, low costs, and staying invested through market cycles—not from sophisticated strategies. |

What Is Asset Allocation and Why It Matters

Asset allocation is the process of dividing your investment capital amongst different asset classes—primarily equities (stocks), fixed income (bonds), and cash equivalents. Each asset class behaves differently under various economic conditions, and your chosen mix determines both your potential returns and the volatility you’ll experience along the way.

The fundamental principle is straightforward: diversification helps reduce your risk without necessarily eliminating growth potential. In investment terms, diversification helps create a more optimal risk/return profile. When equities decline, bonds often hold steady or even appreciate. When inflation rises, certain equity sectors may outperform whilst fixed income struggles. By holding multiple asset classes, you create a portfolio that can weather any market volatility more effectively than concentrated positions.

This isn’t about eliminating risk entirely—that’s impossible if you want meaningful returns. It’s about controlling risk to a level you can tolerate whilst pursuing long-term growth. Asset allocation is how one controls risk, not through market timing or stock picking, but through deliberate portfolio construction.

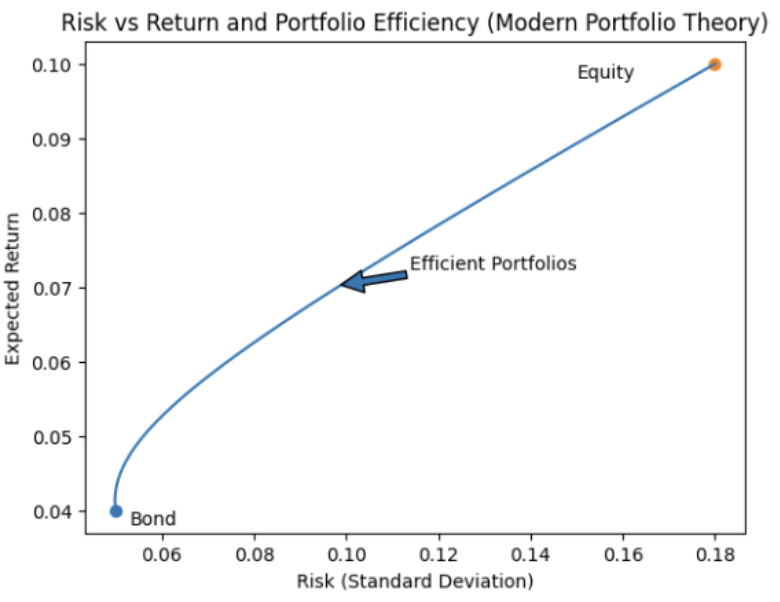

Illustration: In the diagram below, you can see a simple illustration of this concept. Investing all your money in bonds will produce an expected return of 4% with risk of 5%. Investing all in Equities will give an expected return of 10% but with risk of 18%. The arrow points to a portfolio of 50% Equity, 50% Bonds. The expected return is a simple average of 7% (=(4%+10% / 2) but the risk is only 10% (less than the simple average of the risk components (18%+5%/2 = 11.5%). This means a better return per unit of risk. It’s more ‘efficient’.

Risk Vs Return And Portfolio Efficiency (Modern Portfolio Theory)

The maths can prove that the combined portfolio will always be more efficient as long as Equities and Bonds are not perfectly positively correlated (i.e. they don’t always move in the same direction to the same extent at the same time. Very realistic!). The simple conclusion is to never put all your money into one asset class. It’s without justification!

Asset Allocation as Your Portfolio’s Shock Absorber

Different asset classes respond to market conditions in distinct ways. Equities represent ownership in companies and tend to deliver the highest long-term returns, but they’re also the most volatile. During the 2008 financial crisis, global equity markets fell by roughly 50%. During the COVID-19 market shock of March 2020, major indices dropped 30% in weeks.

Bonds, by contrast, are debt securities (like tradeable loans) to governments or corporations. They typically provide steady income through interest payments and experience less dramatic price swings. When equity markets panic, investors often flee to high-quality government bonds, driving their prices up. This inverse relationship makes bonds an effective shock absorber in a portfolio. Although the relationship is not guaranteed to be ‘opposite’, each asset class is affected differently, and it is this lack of perfect correlation that makes the investment portfolio more efficient.

If you want to measure this efficiency you could use a metric such as % return / % risk. Risk here would be measured as standard deviation of the returns. You may end up with a portfolio that generates higher or lower returns than any equity benchmark, but the key is that the ‘return per unit of risk’ would be higher.

Cash and cash equivalents provide stability and liquidity but offer minimal returns, often failing to keep pace with inflation. Their role is less about growth and more about providing dry powder for opportunities or covering near-term expenses without forcing you to sell other assets at inopportune moments.

Your volatility tolerance—your ability to watch your portfolio value fluctuate without making emotional decisions—determines how you should weight these asset classes. A 100% equity portfolio might deliver superior returns over 30 years, but if you sell during the inevitable downturns, you’ll likely underperform a more conservative allocation you could actually hold.

Understanding Your Risk Tolerance

Risk tolerance is often presented as a simple questionnaire result, but the reality is more nuanced. There’s a difference between how much risk you think you can handle and how much you actually can when markets turn against you. Many investors who believed they had high risk tolerance discovered otherwise when their portfolios became painful to hold during real downturns.

Your risk capacity—your financial ability to absorb losses—differs from your risk tolerance. A 25-year-old with stable employment and decades until retirement has high risk capacity. They can afford to hold equities through multiple market cycles. A 60-year-old planning to retire in five years has lower risk capacity, regardless of their emotional comfort with volatility.

The emotional risk of mistiming matters more than mathematical optimisation early on. If you invest heavily in equities and then panic-sell during a downturn, you’ve locked in losses and missed the recovery. A more conservative allocation that you can maintain through market cycles will likely produce better outcomes than an aggressive one you abandon at the worst possible moment.

The ‘Sleep at Night’ Test

The sleep at night test is simple: can you hold your allocation when it’s down significantly without losing sleep or making impulsive changes? If a 30% decline in your portfolio value would cause genuine distress or prompt you to sell, your allocation is too aggressive regardless of what any risk questionnaire suggests.

Consider this practically. If you have £10,000 invested entirely in equities and markets, drop 25%, you’re looking at a £2,500 loss—at least on paper. Can you ignore that and continue with your investment plan? If you have £100,000 and face a £25,000 decline, does your answer change? The absolute numbers matter as much as the percentages.

Risk capacity also involves your investment timeline. Money you’ll need within five years shouldn’t be heavily allocated to equities, regardless of your risk tolerance. The probability of a significant market downturn within any five-year period is substantial enough that you risk being forced to sell at a loss. Conversely, money you won’t touch for 20 years can weather multiple market cycles, making higher equity allocations more appropriate.

The key is honest self-assessment. Many investors overestimate their risk tolerance during bull markets when everything is rising. The true test comes when markets fall and stay down for months or years. If you’re uncertain, start with a moderate allocation and adjust based on your actual emotional response to volatility.

Simple Asset Allocation Strategies for First-Time Investors

Beginners often assume successful investing requires complex strategies and constant monitoring. The opposite is typically true. Simple, broadly diversified approaches using low-cost index funds or ETFs have consistently outperformed more sophisticated strategies for most investors. The mental horsepower required to implement and maintain complex strategies rarely justifies the marginal benefits, if any.

The set-allocation-and-stay-the-course philosophy recognises that your asset allocation decision is more important than any individual investment selection. Once you’ve determined an appropriate mix, the discipline to maintain it through market cycles matters more than tactical adjustments or contrarian approaches like the Dogs of the Dow strategy.

Broad index funds provide exposure to hundreds or thousands of securities with a single investment, eliminating the need to research individual companies. This diversification reduces the impact of any single security’s poor performance whilst capturing overall market returns. For beginners, this simplicity is a feature, not a limitation.

The Three-Fund Portfolio Approach

The three-fund portfolio has become popular for good reason: it provides global diversification with minimal complexity. The approach uses three broad index funds—a domestic equity fund, an international equity fund, and a bond fund. This structure gives you exposure to thousands of companies across developed and emerging markets, plus the stability of fixed income.

A typical implementation might include a total stock market index fund covering your home market, an international equity index fund for global diversification, and a total bond market index fund. The exact percentages depend on your risk tolerance and timeline, but a common starting point for younger investors might be 60% domestic equities, 30% international equities, and 10% bonds.

This globally diverse portfolio using broad index funds eliminates the need for stock picking or market timing. You’re not trying to identify the next great company or predict which sectors will outperform. You’re simply capturing market returns across asset classes whilst controlling risk through your chosen allocation.

The approach contrasts with S&P 500 and chill, which concentrates entirely on large US companies. Whilst the S&P 500 has delivered strong historical returns, it lacks international diversification and excludes small-cap stocks, which have historically provided additional returns. A three-fund portfolio addresses these gaps whilst remaining simple to implement and maintain.

Rebalancing, i.e. periodically adjusting your holdings back to your target allocation, is the only ongoing maintenance required. If equities outperform and grow from 60% to 70% of your portfolio, you sell some equities and buy bonds to restore your original allocation. This forces you to sell high and buy low systematically, without requiring market predictions.

Building Your Portfolio: Lump Sum vs Dollar-Cost Averaging

When you have capital to invest, you face a practical question: invest it all immediately or spread investments over time? This decision often causes more anxiety than it should, particularly for beginners worried about buying at a market peak.

Lump sum investing—deploying all available capital immediately—typically produces better long-term returns mathematically. Markets trend upward over time, so money invested today has more time to compound than money invested next month or next year. Historical analysis consistently shows lump sum investing outperforms dollar-cost averaging roughly two-thirds of the time.

However, dollar-cost averaging—investing fixed amounts at regular intervals—reduces the emotional risk of market timing. If you invest £10,000 today and markets drop 15% tomorrow, you’ll feel like you’ve made a mistake, even though you had no way to predict the decline. If you invest £1,000 monthly over ten months, you’ll buy some shares at higher prices and some at lower prices, averaging out your entry point and reducing the fear-factor.

When Each Approach Makes Sense

The choice between lump sum and dollar-cost averaging often comes down to psychology rather than mathematics. If you have a lump sum available and can genuinely ignore short-term volatility, investing it immediately is likely optimal. The sooner your money is invested, the sooner it can compound.

Dollar-cost averaging makes sense when the emotional comfort it provides prevents you from making worse decisions. If investing a lump sum would cause such anxiety that you’d constantly monitor your portfolio and potentially sell during a downturn, spreading investments over several months is the better choice. The slight mathematical disadvantage is worth it if it keeps you invested.

Your emergency fund situation also matters. Before investing any lump sum, ensure you have adequate cash reserves for unexpected expenses—typically three to six months of essential expenses. Without this buffer, you might be forced to sell investments at a loss to cover emergencies, undermining your long-term strategy.

For regular savers investing from monthly income, dollar-cost averaging happens automatically. You’re not choosing between lump sum and periodic investing—you’re investing as money becomes available. This natural dollar-cost averaging is one reason why consistent saving matters more than perfect market timing.

The long game perspective is crucial here. Whether you invest a lump sum today or spread it over six months will matter very little in 20 years. What matters is that you invest consistently, maintain your allocation, and avoid panic-selling during downturns. Don’t let the lump sum versus dollar-cost averaging decision paralyse you into inaction.

Common Risks and How to Manage Them

Asset allocation models carry inherent risks that beginners must understand. The primary risk isn’t choosing the “wrong” allocation—it’s abandoning your chosen allocation at the worst possible time. Becoming a bagholder—someone stuck holding depreciated assets—happens when you buy high, panic during downturns, and sell low.

Market timing risk affects all investors but particularly beginners who lack experience with market cycles. The temptation to reduce equity exposure when markets feel overvalued or increase it after crashes is strong, but consistently mistiming these moves destroys returns. The emotional risk of mistiming often exceeds the mathematical risk of maintaining a consistent allocation.

Concentration risk—having too much in a single asset class, sector, or geography—can amplify losses. This is why globally diversified portfolios outperform concentrated positions over time. Even if your home market has performed well historically, future returns aren’t guaranteed, and diversification provides insurance against regional underperformance.

Why Saving Rate Matters More Than Allocation Early On

Here’s a mathematical reality that many beginners overlook: asset allocation matters less when portfolio values are small. If you have £5,000 invested, the difference between a 6% return and an 8% return is £100 annually. If you can save an additional £2,000 that year, you’ve added 20 times more to your portfolio than optimising returns would have achieved.

This is why experienced investors often advise beginners to focus on saving 25%+ of income rather than obsessing over allocation details. Early in your investment journey, your contributions dwarf your returns. A disciplined saver with a mediocre allocation will accumulate more wealth than an inconsistent saver with an optimal allocation.

This doesn’t mean allocation is irrelevant—it means keeping it in perspective. Choose a reasonable allocation based on your risk tolerance and timeline, implement it with low-cost index funds, and then focus your energy on increasing your savings rate. As your portfolio grows, the allocation decisions become more impactful, but by then you’ll have more experience and confidence.

The balance between building capital and learning investment discipline is important. Starting with a simple allocation teaches you how markets behave and how you respond to volatility without risking large sums. This experience is valuable when your portfolio reaches sizes where allocation decisions have more significant pound-value impacts.

Target date funds offer a solution for those who want to focus entirely on saving. These funds automatically adjust allocation from aggressive to conservative as you approach a target retirement date, eliminating the need for ongoing allocation decisions. Whilst they’re not perfect, they’re far better than analysis paralysis that prevents you from investing at all.

Common Interview Questions on Asset Allocation

For those working in or entering financial services, you’ll need to discuss asset allocation concepts with colleagues and clients.

How would you explain asset allocation to a client with no investment experience?

Focus on the shock absorber analogy—different investments respond differently to market conditions and mixing them creates a smoother ride. Avoid jargon like “efficient frontier” or “Sharpe ratio” unless the client demonstrates interest in technical details. The goal is understanding, not impressing them with terminology.

What factors determine an appropriate equity-to-bond ratio?

Age and timeline are starting points, but they’re not the complete picture. Risk capacity (financial ability to absorb losses), risk tolerance (emotional comfort with volatility), income stability, existing assets, and specific financial goals all matter. A 30-year-old with stable employment and no dependents can typically hold more equities than a 30-year-old with irregular income and young children, even though their ages are identical.

Technical and Practical Questions

How do you balance theoretical risk models with client psychology?

Acknowledge that mathematically optimal allocations mean nothing if clients abandon them during downturns. A 60/40 portfolio that a client maintains through market cycles will outperform a 90/10 portfolio they panic-sell from during a crash. Your role is finding the most aggressive allocation a client can realistically hold, not the most aggressive allocation they think they want.

How would you address a client who wants to time the market?

Acknowledge the temptation whilst explaining the evidence against it. Even professional fund managers rarely time markets successfully, and the cost of being wrong—missing recoveries or selling before further gains—typically exceeds any benefit. Redirect the conversation towards factors they can control savings rate, costs, tax efficiency, and maintaining discipline.

How do you determine when to adjust a client’s allocation?

Life changes—marriage, children, job changes, approaching retirement—warrant allocation reviews. Market movements alone shouldn’t trigger changes. If a client’s risk tolerance or capacity changes, adjust accordingly. Otherwise, maintain the allocation and rebalance periodically. The wiggles in the curve of market performance are noise, not signals requiring action.

Asset allocation for beginners ultimately comes down to a few key principles: understand your risk tolerance honestly, implement a simple globally diversified strategy, focus on consistent saving, and maintain discipline through market cycles. The investors who succeed aren’t those with the most sophisticated strategies—they’re those who can stay the course when markets test their resolve.

An experienced finance and training professional and Co-Founder of Capital City Training Ltd, Greg has a demonstrated history of working in the financial services sector and has a passion for sharing his knowledge and skills throughout the financial services sector. He has been partnering financial and corporate clients in designing and delivering applied financial programs that make an impact on business outcomes. Greg is skilled in accounting & financial analysis, derivatives and risk management, financial modelling, business valuation and corporate finance and has worked with the worlds leading financial institutions. A strong business development professional and a qualified accountant (ICAEW member), CFA Charterholder and Associate Member of the Association of Corporate Treasurers in the UK (ACT).